Juiced Performance

Sometimes one need only look at the circumstances to determine the results are juiced. Barry Bonds, Lance Armstrong and this guy. Hopefully you’ve not been dieting on bull testicles and dried animal organs for the past couple of years striving to live your best “primal” life, only to be disappointed in the results. I’m no body builder, but at a glance, and absent any knowledge of this man’s history and supposed development of his physique, I’d instantly conclude one thing: juice.

It turns out juicing is everywhere, even in commercial real estate. You see, results are not always what they seem. There’s a common practice, for example, of “buying up” net operating income (“NOI”) by structuring a transaction to have a higher rental rate by giving more concessions (free rent and tenant improvement allowance). Why do this? Well, because it can pay off in the form of increased capitalized asset value on a sale since NOI is a big determinant of asset value (e.g., higher NOI, higher value). You could have two buildings, comparable in every way, both for sale at the same time but having a significant difference in capitalized “value” because one of the owners structured the leases with higher face rates and more concessions and the other achieved lower rents but funded less in concessions. From the occupier’s perspective, where most companies are looking at total occupancy cost, which includes rent and capital spending and considering most companies will use GAAP accounting to straight line the rent expense, the impact of a lease with an artificially high rent but more concessions is a relative wash to one in which the rate and concessions are at market. But this juicing of the results does have longer range negative impacts. Firstly, it results in a higher valuation at sale, translating to a greater tax increase, which in the context of San Francisco office leases is most always passed on directly to the occupier, resulting in higher rent. Secondly, articially inflated rents have the effect of raising the overall base value of the market, making it more expensive.

Of course, a lease is a complex financial transaction which has many variables, including term, rate, landlord funded concessions (free rent and tenant improvements). The market is whatever the counter parties make it. But make no mistake, financial engineering, or “juicing” is everywhere. Given the significantly changed outlook for global office, investors will be less agreeable to paying premiums for juiced performance. How will they know? It’s in the leases; which, like a sample of the Liver King’s bloodwork, will clearly show the juice.

40% Office Availability: Why It's Possible and What It Means for San Francisco

40% Availability

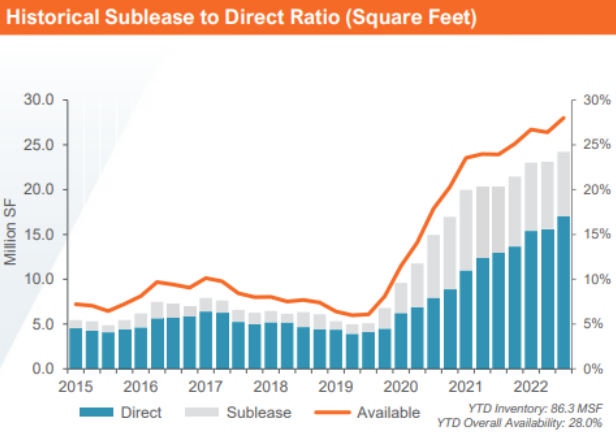

The San Francisco office market consists of 86.3M sf. Presently 28% of the market is available for lease, including both direct space and sublease space, for a total of just over 24M sf. We’re on pace to finish the year with available supply of 30%. The trend in demand (downsizing) and the near certainty of continued macro-economic headwinds in 2023 make it likely we’ll add another 3% to 5% to available supply by the end of ‘23, bringing total availability as high as 35%. It’s too early to predict what 2024 will bring (hopefully a hockey stick graph showing increased demand for office space), but we believe it’s quite possible we’ll see available supply at or near 40%.

We want to talk about this because 30% to 40% available supply is a staggering amount of space (40% is 34M sf). Under normal market circumstances available supply fluctuates (at least partially) due to the introduction of new buildings. These days, supply is increasing exclusively as a byproduct of reduced demand, not new buildings. Positive net absorption is when the amount of available supply is reduced from one period to the next (e.g., quarter to quarter or year over year). Since 2020 we’ve had large amounts of negative net absorption, including this year and very likely next. A healthy market, one in a state of equilibrium, has available supply of around 10%. From 2012 through 2019, net absorption averaged 1,364,942 sf per year. During this period, we had a low of (347,970) in 2017 due to supply additions and a high of 4,838,667 in 2018, the apex of demand during the last cycle. A year in which we achieve 2M sf of positive net absorption in San Francisco would be above average. Consider that it would take 12.5 such years to lower market availability from 40% to 10% (e.g., to absorb 25M sf). What does this mean? It means the impact of all that’s happening now will have a long tail, a period during which despite improvements in the economy and increased demand for San Francisco office space, the volume of available supply will result in a prolonged period of market softness.

For some owners there simply won’t be a pathway to successfully navigate this market and survive to fight another day. And even as buildings trade at much lower valuations, some percentage of supply will remain unleasable as limited demand will naturally gravitate to the best product first. This is when the asset conversion discussion will accelerate. But this, too, is a tricky dynamic because the same problem that’s causing so much supply in the office market (e.g., lack of people coming downtown to occupy office buildings) is also making it less desirable to live downtown, plus it’s expensive to convert product type and not all buildings lend themselves to such conversion (not to mention the backdrop of a declining housing market).

With so much at stake in both the public and private context, it’s important for stakeholders (building owners and government) to take a sober view of potential market performance in the coming years. We appreciate a hopeful outlook as much as the next person, but it’s time to start aggressively planning for more dire outcomes (you know that old saying, “hope for the best and prepare for the worst”). After all, we’ve got enough data now to acknowledge several facts. Firstly, we know there is a reset underway in terms of where knowledge-based workers work. Corporate sentiment about remote work will continue to fluctuate, but hybrid work is here to stay and the continued adjustment by occupiers to hybrid workplace solutions will result in less demand for office space. Adding to the workplace reset, we’re also experiencing a broad repricing of assets, including of company valuations both public and private. Now that capital is expensive and difficult to acquire, companies are no longer focused on the growth at any cost approach. The new objective is profit. This transition requires cost reduction which often begins with the 2 largest expenses: people and real estate. This means less office space.

Market participants can’t “hope” their way through this. For owners of all but the most premium office assets, success will require swift and decisive action to get ahead of rapidly declining market fundamentals by pricing available supply correctly and spending at the asset level to create best-in-class amenities. We personally believe the most successful owners will also establish a variety of ways in which demand can engage with their asset, from traditional leasing, to coworking to flex leasing. City leaders must do all they can to prepare for a long winter of declining tax revenues and increased challenges in promoting and supporting downtown San Francisco. This means spending on the right initiatives to ensure a safe and attractive downtown, while working closely with investors to cut through red tape and support all manner of creative solutions. It’s going to take the entire community, leaders from both business and government, working closely together to navigate this time of significant change.

There is something different on the other side of this. We continue to be hopeful we’ll emerge from this period of change with a new, more vital downtown marketplace. How so? Well, for starters, downtown may become less office-centric, a more holistic place with buildings that serve as hubs for residential, work and retail activities. Green space might become more prevalent as transportation patterns change with more people walking and cycling. Indeed San Francisco’s future downtown has a chance to become a more compelling place, one that accentuates the natural beauty of the surrounding hills and bay while supporting a more diverse spectrum of life and work. It’s way easier to simply hope that things will revert to the way they were in 2019. But the evidence strongly suggests this won’t happen. We’ll all be better off if we begin to focus the collective genius of this great region on defining what’s next.

The Great Reset

Ever consider how odd it is that “great” is the adjective of choice for some of our most challenging times? The Great Depression, The Great Recession, etc. Reflexively, when I think about what’s happening in the office market, the reset that’s playing out all over the world, the first adjective that comes to mind is “great”. Sorry about that.

Let’s also talk about “reset” for a moment. It feels a bit flimsy. Despite being a delicate word choice, it does convey the basic concept. Both sides of the market are resetting. This is the kind of reset where things end up being different than they were, not where we go back to a familiar place and start again. It’s more like a reshaping. We are certain that when the dust settles, the markets will look different.

How? The catalyst is changing demand. Demand for office space is changing in three important ways:

It’s getting smaller

It’s afraid of commitment

It’s way more likely to “swipe left”

The net effect of these changes is a substantial uptick in vacant office space. This, in turn, causes changes to supply as investors compete to fill their buildings. Key changes we’re beginning to see (and which will accelerate) include:

Newer, better amenities

Flexible leasing options

More concessions and lower rent

While this Great Reset thus affects both the product and the consumer, the economic outcome is vastly different for each. In many markets, the occupier (consumer) will enjoy plentiful options, significantly lower costs, a better product and more flexibility - - - so it’s a net positive. Yet the product side (building owners) faces significant challenges. Take the San Francisco market, as an example. Many investors bought assets at pricing that no longer makes sense given market fundamentals. And while the math is bad even without having to invest fresh capital to make the asset competitive, many must do so to be relevant in a 25%+ vacant market. This puts the entire investment thesis in question. Do you double down on the investment, take your pain and hope the market will recover such that you can at least break even (and how realistic is that); or, do you cut your losses now and sell? We think many will sell at steep losses. Why steep losses? Because whereas the seller bought the asset at a time when average rents were $85/sf, vacancy was <7%, demand was strong, debt was cheap and plentiful and rents were increasing 3%-5%+ year over year, the new buyer is investing when average rents are in the $60s and declining, vacancy is >25%, demand is way down, debt is expensive and hard to get and near-term rents are projected to decrease year over year for the foreseeable future. This is precisely why, for many assets, values will decline by 25% or more. The product reset is a modification to the physical offering (more amenities, etc.), a modification of the financial structure (debt and equity), and a modification of the types of leases being offered (flex, etc.). The Great Reset has begun but don’t expect it to proceed smoothly. The consumer has so far proceeded with extreme caution and investors are rarely quick to take losses. But proceed it shall.

Flexing

Over the past couple of decades the long term office lease has become increasingly challenging for occupiers. Demand for space has always been cyclical, rising and falling with the economy, and technology has continued to make it easier for workers to be productive from anywhere. While shared space, or coworking solutions have been around for decades, the scale of the industry expanded rapidly during the period from 2010 to 2020, especially through the Softbank-funded expansion of WeWork. Coworking is a form of flex leasing that is characterized mostly by spaces that are broken into component parts, offering members shared access to services and amenities. The space between coworking and long term direct leasing of separately demised office space is a relatively new place in which a tenant can secure a flexible lease (shorter term of 6 months+) on a fully demised, prebuilt, furnished space which does not include managed services. This is the latest and perhaps most consequential form of flex leasing.

As a product category, these types of flex leases have been slow to emerge primarily because of the historical financial structure of office building investment which targets long term, stable cash flows and risk avoidance - - - effectively the opposite of flex leasing. In contrast, short term flex lease models, by design, expose the landlord/operator to ongoing risk of turnover. Yet what is becoming more clear is occupiers are willing to pay a premium to secure flexible lease alternatives.

The majority of flex space is presently controlled by third party operators, those who take a direct lease from a landlord, create the flex offering and look to sublease it to occupiers at a profit. These operators have essentially proven the business model. Given the high vacancy and declining rents challenging landlords today, we anticipate an acceleration in new flex space options being offered directly by landlords, sans 3rd party operators. This will benefit occupiers in several ways. Firstly, when there is no middleman, the cost of the flex solution will be lower. Secondly, as more landlords enter the market, flex supply will increase. Lastly, office buildings will become more versatile, offering occupiers a variety of leasing solutions ranging from long term, to coworking to flex.

This is an important time of significant change in how investors shape the office product to meet evolving occupier needs. For the first time in the past century, companies will enjoy a broader array of leasing options, enabling them to be more targeted in their commitments. Flexibility will be the single most important objective of nearly all companies as they craft their future workplace plans.

It's Time to Take Action

In 2020 most companies forced their workers to a fully remote posture. In 2021 companies started encouraging their employees back to the office, most with limited success. In 2022 this strained dialogue about return to office has continued. While some have sought to fully address the new realities of the workplace by developing and committing to an approach that both clearly addresses expectations for employees and supports these expectations with modifications to the physical workplace, many have chosen to communicate “soft” messaging about return to office while not making any changes to the physical office.

Historically, but for large companies having significant multi-market portfolios of leased offices, mid-size companies have not been big buyers of the workplace strategy services we provide. Most of these companies have sought to address their offices by mirroring general sector trends, striving to do about the same as their prime competitors. This collective approach gave a sense of security (false?) around the logic of chosen solutions. “If the average AMLaw 100 occupancy ratio is 400 sf/attorney and we’re at 385, we’re doing great”. But these are different times. Everyone is doing things a little (or a lot) differently. There is no safety in numbers.

It's time for small to medium size companies to recognize the importance of having a specific point of view about the office. Employees want to know their employer has been thoughtful on this subject. They want a transparent plan of action that is connected to the core values of the organization. They need to understand why the strategy serves them and the organization better than the current state (likely an ill-defined hybrid). These days, it’s simply not good enough to say, “…we expect you back in the office 4 days a week beginning January 1st”. It’s also true when leaders begin to think about the role of their offices, they quickly realize their beliefs lack conviction. This is because they’ve not really thought about it. While that’s a scary realization, leaders must embrace the moment. After all, workplace, be it fully in-office, fully remote or something in between, is intended to foster greater success. That’s its purpose.

In our market practice we’re seeing a disturbing trend where occupiers are choosing short term lease extensions of underutilized, dysfunctional spaces. Unless the corporate policy is to return to a workplace approach that is exactly as it was pre-pandemic, these solutions have limited chance of success. In most cases, companies who choose to do these short term extensions actually have a new workplace approach they’re communicating internally, they’ve just not taken the time to translate the approach to physical space(s). This is even worse since the physical space is seemingly disconnected from the new strategy. To be fair, for companies who faced lease expirations in 2020, or perhaps early 2021, this was a reasonable approach. The message to employees was, “…we still believe in the importance of the office, but we recognize the fluidity and scale of change in how we and others are using the office and we want to formulate a new, thoughtful approach that is custom designed to help each of you do your best work and by extension, make our organization thrive. For this reason, we’ve elected to do a short term extension of the existing lease while we develop our new approach”. Now however, over 2 years in, this approach sends a strong signal that leadership has failed to be thoughtful on this important subject. Make no mistake, how companies address their offices at this pivotal time will have material implications on their ability to retain and attract talent. It’s time to take action.

Suits, Ties, and the Office

I have a lot of suits and ties. The ties are folded neatly in a drawer that I rarely open. Some are solid, some have stripes, some have little animal prints. I also have a lot of suits. These are mostly tucked into the back of my closet. Oh, I have some expensive leather shoes in a variety of styles, as well. These, too, are stored in various states of disuse. I no longer wear this stuff (but for rare exceptions). The ties were the first to go. I stopped wearing them sometime around 2015/2016. At that time, I still wore suits and nice shoes, just no tie. Shortly thereafter, the suits were replaced by sport coats and slacks. These were still tailored, not casual. But then, at some point, everything became more casual. The nice leather shoes were traded in for the new style sneakers that everyone now wears, or Allbirds or some other more casual footwear. These days I may not even wear a sport coat. Vests are a nice option. They’re flexible and nearly always sure to fit in with the prevailing attire of the day. Plus they make me look sporty, or maybe techy. A little more like I get it (even though I probably don’t).

What’s this got to do with office space, you ask? Behaviors change. If you told 1991 me that 2022 me would show up at work in khakis, a shirt and sneakers, I would have laughed so hard my silk suspenders would have come undone. But here we are. Lately I’ve been wondering, is the office of 2022 like the suit and tie of 2017? In 2017 I occasionally wore a suite and tie, but I had the flexibility to choose not to. In 2022, many employees occasionally go to the office, but they have the flexibility to choose not to.

When I graduated from college I was given “Dress for Success”, a book offering vital guidance on how an aspiring young professional should dress to be taken seriously in the workplace. Although broke, upon getting my first job in the brokerage industry, I was promptly instructed to buy a number of suits (navy or grey), shirts (solid white or blue), ties (solid or striped) and Allen Edmunds cap toe shoes (black). During this period of my life, the office was where I went to experience the physical embodiment of everything I was striving to be professionally. It was a stimulus-rich environment, full of sensory cues that fed my desire to learn. It was in the office that I learned who was powerful and who was not. High on caffeine, I learned the pathways to success (or at least success as it was defined in that office at that time in that market). Did I have what it takes? It wasn’t clear. But if I was going to succeed, it would most certainly require emulating those who were successful. The office was a proving ground. The idea that I could somehow prove myself without physically being there was inconceivable. I had to not only be there, but be there more than all my peers. Lacking experience and skills, I realized the only thing I had to offer was hustle and time.

Young professionals entering the workforce today aren’t likely to harm their careers by not having read “Dress for Success”. Indeed, they can save thousands of dollars not having to dress like they belong in the boardroom. But if we shed the office like we did the suit and tie, how will younger generations learn to succeed? Is this even a real question, or am I just too old and biased based on my experiences? Is there some alternative pathway (Zoom meetings) that will replace the smell of fresh coffee and the experience of watching the office’s best performers do their thing? David Solomon at Goldman Sachs has spoken extensively about the intrinsic and irreplaceable network values Goldman creates through its offices. It’s clear he sees this as a secret sauce ingredient, vital to the firm’s success.

As I navigate the changing world of workplace, I’m becoming increasingly concerned some companies are failing to fully appreciate the many values a thoughtful office can bring to their organization. I don’t blame them, many are still hardwired to think about office space as an expense, not an investment. But it seems to me corporations gave more thought to rolling out Casual Fridays than they’re giving to hybrid and remote work. I confess becoming a bit nostalgic when I see photos of San Francisco in which men are all wearing suits and ties. I’m hoping I won’t one day soon look back at images of people working in office buildings and feel the same. More likely, as we settle into our new normal, some companies, having been quick to embrace a virtual-first posture, will learn the downsides of not having offices. Maybe this is just all part of a healthy exercise in learning what really matters about the office? Certainly elements of the pre-pandemic office (e.g., benching) were about as useful and practical as the tie. My optimistic interpretation of what’s happening now is that we are on a transformational journey to a time when the office will be a place designed to fulfill very specific purposes, a physical space that is understood for the value it brings to the organization. These will be better days for the office. As for the suit and tie…I’m not so sure.

Tech: Big and Small

For decades the San Francisco office market was a unique and seemingly irreplaceable technology hub. The city had so many variables essential to startup tech success that companies believed they had to be here, regardless of the cost. Proximity to Stanford and UC Berkeley, the epicenter of venture capital on Sand Hill Road, the Silicon Valley - - - home to major tech headquarters, including Google, Apple and Facebook and the abundance of bright young tech talent that flocked here from all over the world to be part of the innovation economy. All this in one place. It was a compelling narrative (and true). The city’s beauty and appeal to younger tech workers was obvious. Like New York City was (and remains) for those seeking their fortune in finance, until fairly recently, if tech was your thing, you had to be in San Francisco.

The first wave of tech occupiers shaping San Francisco and contributing to where we are today was decidedly early stage. In the 1990s efforts to monetize the internet resulted in a new economy we came to know as the “dotcom” economy. These were glorious times. Young technology workers flooded the city seeking their cut of IPO riches. Then, in 2000, it all came crashing down. But no matter, there was still gold in them there hills.

Meanwhile the Silicon Valley, traditional domain of tech hardware companies, had steadily diversified its tenant base, attracting a bevy of large headquarters for the likes of Google, Facebook, Apple and more. Young workers, many of whom lost money and their appetite for the startup world, sought refuge in these large, stable companies. But in the early 2000s, these companies had no interest in opening offices in San Francisco. They were “valley” companies. Yet as the economy continued to grow and competition for labor accelerated, it became clear that having a San Francisco office was critical in the war for talent as it turned out the young talent living in San Francisco wanted to live and work here. Thus began the second wave, one in which the city enjoyed not just robust startup activity, but surging demand from big tech, as well.

The third wave, the period from 2010 to 2020, was the perfect storm. There simply wasn’t enough office space in San Francisco – you couldn’t build it fast enough. Startups had seemingly figured out how to avoid the ugliness of being scrutinized in the public market by staying private in perpetuity (thanks to historically cheap and plentiful capital). These companies would routinely go from 2,000 sf to 100,000 sf in a span of 3 years. Venture sponsors would push their portfolio companies to grow as fast as possible. Growth at any cost. Meanwhile, having long ago established their beachheads in the city, the big tech giants would occasionally rise up and take down space in 300,000 sf+ increments. We even had home grown startups that made it all the way from small to big in the likes of Salesforce, who dominated the city with its bold strategy for a world class campus totaling millions of square feet, smack in the middle of the CBD. More than a few massive real estate deals happened solely because one company was convinced another was about to lease a block of space that stood in their path of growth. This was called “defensive leasing” and it was a developers best friend. The specter of Google or Facebook leasing up a huge swath of space was a bit like Keyser Soze from the Usual Suspects. You could never be sure it was real, but it was possible. And in those times, when hiring was frenetic, having a little extra space was no problem. Hell, if it turned out you didn’t need it, you could probably make money on it downstream…it’s an asset, after all.

This is the story of San Francisco these past 30 years. Three waves of tech overtaking the market, redefining the city with a growth engine the likes of which few cities have ever seen. But today it’s different. We’re in the fourth wave. We have problems at both ends of the tech demand spectrum. On the big end, companies are bracing for a recession, freezing new hires; and, in some cases, laying off employees. When they are hiring, they’re adopting a more distributed approach to labor, looking for higher quality at a lower cost, which often means not in San Francisco. At the same time, the small end of tech demand spectrum, the startup world, has taken its show on the road. VC spending is both down overall and, importantly, down in the region. We have a lot of vacancy – currently 23%, a record high. We know the coming quarters will bring more vacancy as expiring leases will result in reduced amounts of leased space. With the San Francisco startup engine turned off and Keyser Soze long since gone, how will the technology sector absorb all this excess space? Or, will this fourth wave stand as a time when our great city is forced to pivot to a more normalized office market, one in which demand is more diversified, less tech heavy and occupiers have abundant space options? What would that look like? For starters, the underlying rental values would be substantially lower and would remain so for a prolonged period of time. But for limited market segments, when the market has a vacancy factor north of 15%, it’s generally a tenant’s market. Despite being 2.5 years into the pandemic, the story of the San Francisco office market’s fourth wave is still young. And just as with the prior three waves, this one will be no less fascinating to experience.

Let's Exchange Financials

The price of San Francisco office space is mostly falling. Sure, there’s some outlier examples of premier view space where the price is stable, even increasing. But, on balance, we’re talking about a significantly declining market. A silver lining for occupiers who’ve otherwise endured a long period of limited supply and record high costs. Yet while on paper the cost of the market looks better, the effects of the downturn can (and will) render some landlords incapable of effectively running the building. Because most lease negotiations are set up as a sort of “David and Goliath” battle in which the tenant is David and the landlord Goliath, it’s not necessarily common for tenants to ask too many questions about a landlord’s financial position. Yet like the tenant, the landlord has many obligations under the lease, the performance of which require its financial health. Tenants must share their financials and often provide security mechanisms to secure their performance under the lease. This typically comes in the form of a letter of credit or security deposit. The landlord version of security for the tenant would be things like a self-help provision and/or an SNDA. Self-help enables the tenant to solve for issues the landlord is otherwise obligated to solve, but for which it does not have the capital to do so, by paying to have the work done and deducting the cost from Rent. The SNDA, or subordination non-disturbance agreement, is a legal document that protects the terms of the lease in the event a lender takes over building (e.g., the landlord defaults on the loan). These are examples of protective mechanisms against a failing landlord.

It’s generally true that larger institutional landlords are better positioned to perform through cycles, maintaining the operational integrity of the asset despite a market downturn. Quality landlords run the asset with a constant eye on maintenance and performance. Where possible, they invest to enhance the building’s performance and to ensure the longevity of the equipment and systems. However, when faced with mounting vacancy and reduced or even negative returns from leasing activity, corners may be cut. Rarely does this work out in a way that isn’t impactful (negatively) to the occupants. Maybe it’s the elevators that were slated for mechanical upgrades prior to the downturn, but have now been put on hold. Or, perhaps it’s the chiller, which in the absence of being replaced or properly repaired is now prone to stalling out when the temperature hits 80 or higher…right when you need it the most. We’ve seen examples over the years when the “landlord” with whom we are supposed to negotiate has actually lost all its equity and the debt holders are trying to figure out what to do with the asset. This can be precarious because the party with whom you are negotiating may not actually be able to bind the landlord. Remarkably, most landlords in this situation won’t volunteer their deficiencies in this regard. This means a tenant could go all the way down the path toward a transaction, negotiating in good faith with the “landlord”, only to have the terms rejected by the lender (the actual landlord).

Now is an excellent time to secure a long term cost advantage for San Francisco office space. But it’s also a time to be cautious and to know the landlord’s financial position. It’s a time when negotiations may veer into the realm of the uncomfortable, but with good reason. After all, a lease is about much more than Rent. Having the right protections in place to navigate the landscape of a steeply declining market is critical to your success and peace of mind as a tenant. And make no mistake, we’ve now entered a time in which there will be those who can no longer adequately operate the asset. Just because the building is a big asset and the landlord a big institution does not mean it’s well positioned. Right now there are assets in downtown San Francisco (and most major US Metros) that have debt levels which are higher than the market value of the building and for which the leasing potential will yield results that generate a negligible or even negative net return.

What's Possible?

When it comes to negotiating with landlords for office space, today the San Francisco market and many like it officially fall in the “…it doesn’t hurt to ask” zone. In this rare market space, occupiers have the luxury of translating their concerns as challenges for landlords to solve, or not. This includes many challenges that stood zero chance of being addressed (or even considered) in the years prior to the pandemic.

Examples include things like termination rights, contraction and expansion rights and even future downward adjustments to rent if the market for comparable space and/or space in the subject building declines in value. Indeed, these types of challenges may prohibit a tenant from transacting, or from transacting for a longer term commitment, creating even stronger headwinds in an already difficult market. Take the scenario in which the occupier is uncertain about the amount of space it will require over a 5+ year time horizon (by the way, nearly every occupier we talk to is struggling with this uncertainty). They can estimate the current need, but it’s often based on low usage. So they attempt to project a more stabilized occupancy need. But to do so, they have to make assumptions about return to office which they fully recognize may play out differently than projected. They need a lot of flexibility to adjust the amount of leased space over time. The winning landlord may thus be the one that provides the greatest amount of size flex. Then there’s the question of rent. It’s hard for companies to execute long term lease commitments today when the market has turned, but is clearly poised to drop more (possibly much more). Nobody wants to sign a lease only to see the value of comparable space fall precipitously. The investor who can help the tenant avoid this outcome stands a better chance of securing the tenancy. Why would a landlord provide so much flexibility? Because they have to.

It’s important to note how unusual these times really are. This is a moment in time when occupiers can just say “no thanks” and walk away, unburdened by a lot of the traditional pressures that drove decisions, including the need to solve for an expiring lease. With reason to believe the near term market will only get better, meaning it will offer more options at lower costs, there’s limited incentive for occupiers to sign long term leases. This is why we believe the realm of what’s possible is about to get a whole lot more expansive. Don’t get me wrong, it won’t come easily. But when the challenges are thoughtfully presented as opportunities for competing landlords to provide solutions, and the absence of such solutions stalls leasing activity, we believe the landlord market will get creative. So don’t assume your problem can’t be solved. Odds are it can.

Market Leverage, Mass Psychology and the San Francisco Office Market

In the context of lease negotiations, counter parties seek to leverage market dynamics to maximize their advantage. For office markets, the primary dynamic being leveraged is that of supply/demand. When supply is scarce and demand is strong, the landlord counter party leverages scarcity to increase rents and reduce concessions. Alternatively, when supply is plentiful and demand is low, tenants leverage their options to lower rent and increase concessions. Basic stuff, right? Perhaps more interesting is the mass psychology that evolves around a marketplace which has experienced a prolonged run of one-sided leverage.

In the decade prior to the onset of the pandemic, available space in San Francisco became increasingly scarce as demand skyrocketed. During this period market participants accepted certain market behavioral characteristics as normal, indeed necessary in order to transact. This mass psychology was initiated and enforced from the landlord’s side of the negotiating table, as it was they who enjoyed the leverage. To a new occupier-side participant, say a company that was new to the market, the mass psychology here seemed insane. To these participants, the uninitiated, it was a struggle to understand how the landlord counter party could be so unreasonable, so inflexible. In other words, despite the dynamic feeling normal to those having historical market context, it was quite abnormal to all others.

That’s what mass psychology does. It makes otherwise extraordinary situations seem normal. This same effect enabled investors to rationalize ever increasing acquisition pricing with the belief that markets would continue to rise. In essence, the more the leverage dynamic tilts one way or the other, the less rational the mass psychology becomes. So it was that we saw more than a decade of market mass psychology that heavily favored investors at the expense of occupiers. Now the narrative is shifting (rapidly). Market leverage, but for isolated and limited instances, is squarely in favor the occupier. What’s interesting is how hard it can be for the counter party who previously enjoyed favorable leverage to recognize and accept a shifting landscape. Today landlords will react with incredulity when they’re met with aggressive proposals from the occupier counter party; this notwithstanding more than a decade of a “take it or leave it” negotiating posture. It’s interesting to observe. Don’t get me wrong, I understand the implications, I understand why one party or the other might find elements of a negotiation challenging. But like it or not, the foundations of a new mass psychology are being established across global markets, certainly here in San Francisco. Included among the things all participants will soon find “normal”:

Long RFPs in which landlords are graded on the extent to which they address all factors

Occupier flexibility that exceeds the limits of traditional lease underwriting (e.g., capital spend vs. lease term)

Long periods of downtime

Large amounts of vacancy

Scrutiny of landlord debt and equity

Self-help provisions

Prop 13 tax protection

Most Favored Nation clauses

Termination, contraction and growth rights

Progressively decreasing lease values (the inverse use of lease comp data from when rents were climbing – meaning tenant advisors look to achieve X% lower than the most recent comparable values as opposed to landlords seeking to achieve increasingly higher values)

In some cases, negative NERs (e.g., money losing leases)

Creative problem solving

Excessive capital contribution including turnkey scenarios

There will be market leading deals that drive the markets to new lows, much as there were such transactions that defined the new highs during the boom times. The most desirable occupiers, those having the best credit and leasing the largest spaces, will exercise outsized leverage. It’s difficult to negotiate from a position of disadvantage. But successful owners will embrace this new reality, accept their market position, embrace the mass psychology and do what they must to get deals done. In fact, those who resist less, will enjoy more

Find Your People Then Build Them a Place

Every industry and company has unique labor needs. These needs can be synthesized into target demographic profiles which can be used to evaluate global markets in search of the best places to grow the business. Certainly there is more that goes into where a company elects to establish a presence than just the amount of available talent. Among other factors, companies might consider proximity to key clients, proximity to investors (e.g., venture capital), proximity to educational institutions graduating the target demographic, cost of living, cost of office space, government incentives, even proximity to competitors from whom talent may be poached. Indeed, discovering the best markets is a complex undertaking.

Labor analytics has become an increasingly vital (and common) part of our service offering. Yes, we’re a real estate services company. But when it comes to how we advise our clients on the subject of workplace, it’s really about people. And to get “people” right you need to begin by identify the best places to find your people. Even the best physical workplaces will fail to fully realize their benefit to the business when located in the wrong place (e.g. access to talent is not fully optimized). When companies get it right they access more and better talent, creating a competitive advantage over industry competitors. Today we see strong interest from our clients in understanding what their industry peers are doing about the physical workplace as they struggle to define their own path forward. But the focus of their interest should really be where, not what; as in, where has the competition chosen to locate its offices? This study will begin to reveal patterns that center around concentrations of the type of labor that is essential to success in a given industry.

The traditional work we do around creating the best workplaces, focused on the building, space and neighborhood that comprise the physical office naturally evolves after full consideration of the labor implications. It’s worth asking why your offices are located where they are. It’s worth considering whether you’re positioned to access the best talent, whether you enjoy an advantage over your competition, or not. Choosing the right market(s) and then crafting the best workplace solutions, ones which promote the health and productivity of the workforce are among the single most impactful actions leaders can take.

Cushman & Wakefield has an outstanding team of labor and incentives consultants. We’re doing great work for companies all over the world. It’s an exciting time to be part of the evolution of workplace, especially to witness how much the focus is shifting to the employee. For the first time in my 30+ year career, companies are viewing this through the right lens, one that prioritizes getting the right talent and giving them the right resources to do their best work.

Why We Write

Why do you get these weekly communications from us? What is TenantSee? We figured it’s time to explain a few things.

Let’s start with the second question first. TenantSee is the name we’ve given to our approach to tenant real estate services. We chose this name because we believe its important for tenants to see more. To see more what, you may ask. To see more of the big picture and the little details that make for better real estate outcomes. To see more of the data and analytics that drive good decision making. To see more transparently, the specific strategies we employ to maximize value. To de-mystify good tenant real estate. For us, the traditional approach to tenant advisory was opaque and failed to get some basic things right, exposing occupiers to an unnecessary knowledge deficit when compared to the landlord counter-party.

TenantSee is 3 things:

A source of tenant-focused content, consistently delivered, free to all

A technology platform for the delivery of our specific approach to tenant advisory and for the management and visualization of critical data

A playbook for creating and achieving optimal leasing outcomes

TenantSee Weekly, what you’re reading now, is one component of our overall approach to communication. In total, we use social media (LinkedIn), our websites www.lowfogg.com and www.tenantsee.co, special events (Café TenantSee), our quarterly market report “The Tenant’s Perspective” and this weekly email to distribute free content. We’ve heard from many of you that you enjoy our content. We appreciate your support, it motivates us to do better. Some from within our industry have questioned why we would provide our insights and perspective so freely? To us, this speaks to the “old way” when tenant real estate services were opaque and involved a transaction between the tenant and broker in which the broker traded information for fees. Today, information is readily available to all – there’s actually too much of it. Our role is to help our clients understand which information matters and to provide them with insights and analysis they can’t generate on their own.

While our content is free, it would be disingenuous to suggest we don’t have a self-interest at play. After all, our goal is to discover and build new relationships by sharing how we think, by helping people understand our particular approach to tenant advisory. Some small percentage of our total audience will ultimately become clients. This is why we write. Hopefully TenantSee Weekly and all the content we deliver is valuable to you. We’re now planning our next Café TenantSee event - - - we’ll be reaching out soon with more details. If you like hearing from us, never hesitate to let us know. It makes our day!

Prop 8 Protection

Prop 8 allows owners to appeal for a temporary reduction in taxes when property values have declined. When granted, the relief is for a period of one year, after which point the owner must reapply. This is a important topic, as given the current state of the San Francisco office market, we anticipate a lot of owners will go to the city seeking relief.

Why do occupiers need to be aware of Prop 8 relief? It’s important because many buildings in San Francisco use a base year lease structure, wherein the tenant is responsible for increases in operating expenses and real estate taxes above a base amount (typically the calendar year in which the lease is executed). With this type of lease the tenant is thus exposed to a potentially large increase in taxes if it does not have a Prop 8 protection clause. Let us explain with an example. Let’s say Company X leases 15,000 sf on a base year lease. The lease is signed in February of 2023 and the 2023 calendar year is the tax base year. At the time of lease execution, the tax value is $6/sf. However, the landlord successfully appeals the taxes and gets the 2023 value down to $4/sf. But this relief only lasts for one year, after which point the tax value reverts to the prior level. The issue is Company X ends up with an artificially low value for its tax base year ($4/sf, the value of the taxes during the base year per the lease). This means that as the asset’s tax value reverts to its pre-relief value ($6/sf), the tenant is hit with a $2/sf tax increase (the same as a $2/sf rent increase). And it continues to pay increases thereafter on the low base year value (meaning its future increase are also larger than they should be). Under Prop 13 in California, but for asset financing activity (sale or loan) relating to an interest of 50% or greater, taxes increase only 2% annually. Absent the landlord’s temporary relief in 2023, Company X’s tax exposure in the subsequent year would have been $6/sf + 2%, or $0.12/sf, or $1,800. Instead, it’s $30,000.

The solution to this problem is simple; and most (if not all) landlords will give it in lease negotiations. It is generally referred to as Prop 8 protection and it states, irrespective of any tax appeals and relief that lowers the building taxes below the base year value, the tenant’s base year shall remain unchanged. If Company X had this protection, it’s base year tax value would have remained $6/sf and, despite the landlord’s successful appeal, subsequent tax increases would have been calculated off the pre-relief tax value ($6/sf). By the way, when a lease is NNN, you don’t have this issue because the taxes are passed through directly at whatever value they happen to be at that time, not over a base year. With so many landlords poised to appeal, this is a must have provision in current lease negotiations.

San Francisco's Demand Problem

The San Francisco office market consists of 86M sf. Currently, 18.7M sf is available, 13.7M direct from landlords and 5M for sublease. This means that 72.3M sf is leased and not being marketed for sublease. We can assume there will not be much (if any) new supply added to the market over the next several years. Demand will be the key factor in determining the market’s trajectory.

In any given year, only a small percentage of the total leased space expires. Of the expiring leases, a small percentage will be for space otherwise available for sublease and for which the master tenant has no interest in continuing to lease. This space will revert to direct vacancy. The big question is what happens with the balance of the leases, whether these tenants sign new leases that are smaller, equal to, or larger than the space leased at expiration.

Our view is market vacancy will continue to increase for at least another year as we see an aggregate reduction in demand for space. How might this play out? For example, let’s say 8% of the leased space (72.3M sf) expires next year. This represents 5,784,000 sf of leased space at the time of expiration. But let’s assume 5%, or 289,200 sf of this space was available for sublease and will not be extended. That leaves us with 5,494,800 sf of potential demand. This demand can grow, shrink or remain unchanged. At this time, we’re generally seeing a net downsize of ~25% to ~30%. At 25%, this would reduce leasing activity to 4,121,100. Of course, there will be some level of net new leasing from companies that had not previously existed and/or whom did not previously have an office in the San Francisco market. Let’s assume this new leasing totals 500,000 sf. These net new leases bring total demand up to 4,621,100. But the overall net effect of this hypothetical year would be to add 1.35% to total vacancy, bringing it from 21.7% to 23.05%.

To be sure, market performance will vary by asset and submarket. But prolonged periods of high vacancy and reduced demand will have a material impact on rental economics, driving down the average cost to lease. Tenants can expect significant leverage, with many options to choose from. For occupiers, this is the silver lining of San Francisco’s office demand problem.

The Restructure

What may not be readily apparent to some occupiers is the extent to which the San Francisco office market presents an opportunity to restructure leases. What does it mean to “restructure” a lease, you may ask. Well, it can mean a lot of different things, but in this case we’re talking about negotiating new terms ahead of an expiration such that the tenant receives immediate benefit. For example, say a lease has 3 years remaining at rents that are significantly above market and the tenant requires improvements to modify the space. If the tenant is willing to commit to the building for a term extension beyond the existing expiration, depending on the circumstances at the asset level, there may be an opportunity to recast the lease. The trade for the landlord is one of near term pain for long term gain. The trade for the tenant is one of near term gain for (potentially) less future gain. In a perfect world scenario, timing would work just right and the tenant would make the trade early, only to see the market turn less favorable thereby making the restructure look genius.

But achieving genius outcomes, while aspirational, is seldom how things actually work out. Hence it’s very important to consider a possible lease restructure in comparison to doing nothing at all. What would the current obligation + a future scenario (negotiated on the timeline of the existing expiration) look like? Is it likely to be more or less favorable than the early restructure? To be sure, the restructure negotiation necessarily plays out with lesser leverage than the tenant would otherwise enjoy if negotiating closer to its natural expiration. This is because of the remaining obligation. So why might an occupier consider attempting an early restructure? Several reasons:

Near term need to reduce obligation

(the benefits of negotiating now for reduced obligation outweigh the longer range benefits that might be achieved by being able to fully exercise leverage)

Near term need for capital to make improvements to the space

(especially relevant as companies think about redoing space to encourage RTO)

Belief the value of a restructured lease, notwithstanding the limits on leverage, will outperform the longer range cost of waiting and negotiating downstream

OK, so why would a landlord make this trade? For starters, there may be significant current vacancy and/or upcoming vacancy from now until the existing lease expiration causing the investors to seek stability. And despite what is often a “bullish” outward facing persona, in down markets (especially this current iteration) many investors are privately concerned. They may have limited confidence in future market performance and place greater value on stability, even if it comes at a cost. Their version of the math may tell them the future, when the tenant’s lease expires, could end up being worse than the present; and/or, even if it’s better, it may not be better enough to risk losing the tenant.

Surprisingly, occupiers often fail to contemplate restructure scenarios, let alone actually making the effort. This is due to a long held belief that the lease is largely fixed for the term and otherwise non-negotiable. Maybe. But maybe not. It may also be due to a lack of thoughtful analysis and/or quality advice. Tenants tend to think of real estate advisors when they think they have a definitive need for such services. They may also feel uncertain about engaging an advisor to underwrite different scenarios as they know tenant advisors are typically paid by the landlord upon completion of a transaction – hence the work necessary to underwrite a potential restructure may be speculative, lacking compensation. To be fair, not all tenant brokers have the resources (research, understanding of landlord motivations, experience) to undertake this exercise in a thoughtful manner.

Here are a few gating issues to consider before assessing a potential restructure:

Is the space suitable for some period of time beyond the existing expiration?

How long (i.e., 3 years, 5 years, etc.)?

Does it require improvements to achieve such suitability?

Is the current rent obligation above current market?

Does the landlord have exposure?

Equity/debt

Vacancy

Other

If the answer to these questions is “yes”, it’s likely worth underwriting possible restructure scenarios. The result of that analysis will inform whether it makes sense to make a bid. The ultimate decision, go or no go, should be made based on the extent to which the negotiated outcome performs positively in comparison to the alternative.

Where's the Exit

The office lease is a complicated contract. Once executed, but for its expiration, there’s no easy way out. In our experience, companies often give too little consideration to the exit. It’s understandable amidst the excitement of signing a new lease. Thinking about how to unwind the lease before signing it is a bit like sliding a prenup across the table to your future bride a few days before the wedding. But things happen. And things especially happen over a period of years.

So how should companies think about the exit? Firstly, they should contemplate business scenarios that might result in circumstances which would render the lease problematic. These would include positive growth scenarios in which the space would be too small; and, downsize scenarios in which the space is too big. How likely is either to occur? What remedies can be negotiated into the transaction to alleviate these scenarios? For example, if there is a high expectation of growth, such growth should be modeled and during the negotiations efforts should be made to secure future contiguous space in the building - - - not necessarily as commitments, but as opportunities or options, such that if the space is needed there will be a solution. Alternatively, consideration should be given to downsize mechanisms which might include everything from termination of the lease to contraction of the leased premises. Of course, most leases have sublease and assignment rights that allow the tenant varying degrees of flexibility. But these are heavily negotiated rights that can be either beneficial or not so helpful, depending upon the quality of the negotiated outcome.

There are many ways to address expansion. The most common concepts include:

Must Take

Right of First Refusal (ROFR)

Right of First Offer (ROFO)

Option for specific amount of space during specific period of time

The Must Take is exactly what it sounds like, a forward commitment to take a certain amount of space at a specific time. The ROFR is a scenario in which the tenant has the right to “refuse” a deal that has otherwise been negotiated with a 3rd party tenant. Landlords don’t like this structure because it is an encumbrance on their leasing effort, one they typically feel compelled to disclose and which can thus impact their ability to lease the space. The most common and least taxing approach is the ROFO. We often see tenants make the mistake of having a “one time” ROFO on existing vacancy. This is a problem because the landlord will offer the space immediately upon execution of the lease (when, of course, the tenant does not need it), forcing the tenant to decline the space and freeing the landlord to lease it without restriction. Hence in certain circumstances, the one time ROFO is of zero value. Better is an ongoing ROFO. Still better is an ongoing ROFO that has a second bite at the apple in the event the subject space is not leased within a certain period of time subsequent to tenant’s rejection. Lastly, there is the option. Options obligate the landlord to provide a certain amount of space within a certain window of time. These are also more difficult to negotiate because they, too, serve to encumber the landlord.

On the subject of downside flexibility, there are essentially 2 scenarios:

Termination Option

Contraction Option

The termination option will be exercisable at a point in time and have a set termination date. It will nearly always call for the tenant to pay a termination penalty which is often calculated as the unamortized cost of tenant improvements and leasing fees (amortized with interest), plus some number of months of rent. Depending upon market conditions, a tenant may find that subleasing yields a better outcome than exercising the termination. As to contraction rights, these are similarly structured, but relate to only a portion of the space.

Finally, there is the most common mechanism for exiting unwanted space, the sublease. Subleasing is a highly market-sensitive outcome. In markets like current day San Francisco, it is extremely difficult. Subleases are often discounted because the subtenant does not enjoy the same rights as a direct tenant, the term is usually shorter than normal and there is typically not much money available for tenant improvements. Subleasing is, at best, an imperfect solution.

Leasing is about more than negotiating a market favorable rent. There’s a lot to consider, including what happens if you no longer need all or a portion of the space. We’re always available to take a deeper dive on any of our TenantSee Weekly topics, just ask.

Landlord Strategies, Oppositional Landlords and Leverage: Random Thoughts

Rent, or net operating income, is 100% correlated with value. When an owner lowers the rent, they reduce the value of their building. This is why many investors will do all sorts of things before lowering rent. For example, the most common approach is to provide big allowances and/or large amounts of free rent in exchange for rate preservation. It doesn’t feel great, but since it protects asset value, it’s in chapter one of every institutional owner’s playbook.

But not all owners have the same motivation, which is why we see so many different approaches to declining markets. Investors who are committed to a long-term hold strategy are generally less concerned with rate preservation (they don’t plan to sell any time soon and may prefer to limit capital spending in favor of lower rents). Most major markets will have a full spectrum of owner motivation profiles and strategies.

At the end of the day, a proper, declining market strategy for the occupier (tenant) will include a broad sampling of these unique owner motivation profiles (e.g., not just institutional rate preservationists). In negotiating with owners, all scenarios should be compared in a comprehensive model that captures total occupancy cost, which includes rent and all other spending. While the rate may be more favorable in scenario A than B, scenario A may also come with a hefty capital requirement (a tenant cost); which, once fully vetted, may render scenario A more expensive than B from a total occupancy cost perspective.

Our TenantSee Weekly topics are usually a direct reflection upon real world events unfolding in our practice from one week to the next. This week, as we think about the different way owners approach declining markets, we’re struck by the failed strategy of Oppositional Landlords (see our earlier writings on this subject in the content library at www.lowfogg.com). These owners often define their negotiating strategy based on drivers that are misaligned with the market (e.g., the owner who refuses to pay a leasing commission). The smart occupier, properly advised, will easily leverage this failed strategy by letting dialogue with the Oppositional Landlord die a fast death, instead focusing on identifying and negotiating relocation scenarios. Should the existing space remain of interest in the context of a lease extension, the tenant may reengage with the Oppositional Landlord at the end of its process. This, of course, leaves the Oppositional Landlord with one move…to undercut the market. Adding insult to injury, these landlords typically lack market data because their market posture isolates them from market participants (notably brokers). They’re forced to compete by blindly lowering the value of their offering. Not good.

Leverage is present in every negotiation. One of the keys to good negotiating is understanding leverage - - - importantly, both yours and theirs. These are some strange times in office markets all over the world, but especially so here in San Francisco. Stay focused and fear not the Oppositional Landlord!

The Space Between...

When it comes to office space, corporate leaders now find themselves stuck in the space between the forced closure of their offices in 2020 and having to conceive new workplace approaches that (somehow) foster productivity, enhance recruitment and retention and (generally) satisfy the diverse (and conflicting) needs of the employees. This is not a comfortable place. Indeed, we’re finding that many corporate leaders are unwilling to take responsibility for conceiving and executing a future workplace strategy. They fear making the wrong decision. Who can blame them? After all, given the extent and pace of change, it seems more likely for future oriented workplace strategies to fail than succeed. Who wants to take on that risk?

Workplace solutions are heavily influenced by industry and geography. For example, the Bay Area tech sector has been among the most aggressive sectors in adopting remote or virtual-first strategies. Corporate behavior is a lot like individual behavior in the sense there is conformity to the norm. When the large companies in a sector or region adopt a particular approach, the medium and smaller firms tend to follow suit. Yet in many sectors and regions, the norm has yet to be established. In fact, it seems like everyone is doing something different, iterating a form of hybrid or other workplace approach, the details of which are murky and therefore hard to replicate. The overall effect is to keep us stuck here in the space between.

For now, we don’t see any easy way out. We expect to see a lot of short and medium term solutions that are made more out of risk avoidance than creative problem solving. Yet all decisions, even a decision to effectively do nothing, have consequences (both intended and unintended). While figuring out how to do things better may be difficult, it’s essential. Near term wallowing in the space between will do little to address what is clearly a new mandate for the future of work. It may feel “safe” in the moment; but, ultimately, it stands to put the organization at a competitive disadvantage and make its leadership seem out of touch.

Thoughts on Broker-Led Solutions for the Middle Market

Finding high quality real estate services is easiest when a company is small, solving for one lease or a few leases in a small region; or, when a company is large and looking to hire a global partner that can provide a spectrum of services for managing a complex portfolio. These are the “bookends” of the market where there is the greatest alignment between the structure of the services and the client need. It’s in the middle, companies of 250 – 5,000 employees, where things get challenging. This week, we’ll explore important considerations when searching for a real estate advisor in this middle market.

First, we need to explain a little about the structure of real estate service firms. Small, independent brokerage firms can often provide excellent transaction related services in a given market. However, these firms are not positioned to do quality work outside their market, nor do they have broad scope capabilities or the resources necessary to address multi-market, portfolio level advisory. On the other hand, large firms (like Cushman & Wakefield) can play in both markets, having capable transaction professionals on the ground in local markets and teams of consultants and corporate account executives who provide full scope services to large scale clients. Yet the big client solution teams and services at all of the large service firms (including Cushman & Wakefield) don’t scale down well. It’s too expensive and cumbersome to activate these services for accounts that generate revenue which is below a certain minimum threshold. Hence the service gap in the middle.

Let’s say your company has 1,000 employees in 25 offices throughout the US, with an average office size of 7,000 sf. You have an average lease commitment of 5 years and an average annual spend of $350,000 per office, or $8.75M. This is a portfolio that deserves a higher degree of service than one-off market brokerage. Every year, you likely have a number of lease related issues to manage (expiring leases, contraction, expansion, M&A, etc.) and you need a system for managing the leases, for creating visibility into the portfolio and for gaining ready access to vital data that can inform good decisions. At this size, you likely have someone from Ops, finance, HR or some combination thereof, responsible for real estate. These folks also have a “day job”. If you are selectively addressing each market independently with local transaction professionals, you’re missing out on broader scope services that could materially improve both the quality and functioning of the portfolio. At the same time, you’re too small to get the attention of the big account platforms. What to do?

The middle market is the largest market segment in the world. You would think the big real estate service providers would have long ago emphasized the development of service offerings that targeted this market. But they haven’t. Doing so requires finding ways to scale down some of the portfolio management solutions these firms provide at the top level, while simultaneously causing a percentage of the local market brokers to scale up their business by becoming skilled at multi-market portfolio advisory. In the absence of well developed offerings, middle market clients often fall prey to what they don’t know (i.e., they don’t know what services are actually available, or how to get them), or to a slick pitch that overstates capabilities. Since the corporate solutions level teams aren’t selling into this market, the usual point of connection is at the broker level. The service platform is thus run by either a broker or a small team of brokers. A common mistake is for the client to hire a broker they like in a given market to run the whole portfolio based on the experience they had in one market, irrespective of whether this broker has the network, skills, resources and scope of services necessary to handle the portfolio.

The first place to start when evaluating a broker-led portfolio solution is to ensure the firm has adequate coverage, meaning do they have offices in the cities where you have space? Secondly, it’s important to understand whether the broker has experience managing multi-market client work. Next, you must assess the scope of services being offered. Does the firm provide lease administration? Do they have portfolio analytics? Do they have market research? How do they engage with the client to proactively provide insights and guidance? What level of quantitative and qualitative analytics do they provide? Can they assist with design and project management? How are their services compensated? This is where the stuff you don’t know can cost you (and the reason for this post). Middle market customers are extremely valuable. It’s common for lower end service providers to offer “financial incentives” to win these clients in the form of fee rebates. Fee rebates, in general, aren’t a good trade for the client. Using our example, let’s say there’s 15% client rebate and the portfolio generates average brokerage fees of $500,000 annually. You get $75,000 in rebates, which you have to book as taxable income. Not much value. What you should be doing instead, is negotiating for the provision of extra services and a platform that helps manage the portfolio and articulate the process to ensure consistency across geography. Many of the same firms who are eager to rebate fee do so because they lack essential services. It’s kind of a “look here, not there” approach.

This is not a commercial for TenantSee, powered by Cushman & Wakefield, but we’d be remiss if we didn’t point out that TenantSee was built specifically to address this middle market. We’re always happy to show our proprietary platform, including custom dashboards built on Microsoft Power BI, and to share how we help our multi-market clients design and execute better real estate solutions. Importantly, as a member of the TenantSee Community, we’re also happy to answer questions or help you think about how to procure the right service solution for your specific need. We’re always mindful that our approach is not a fit for everyone, but we see value in being a resource to all.