40% Office Availability: Why It's Possible and What It Means for San Francisco

40% Availability

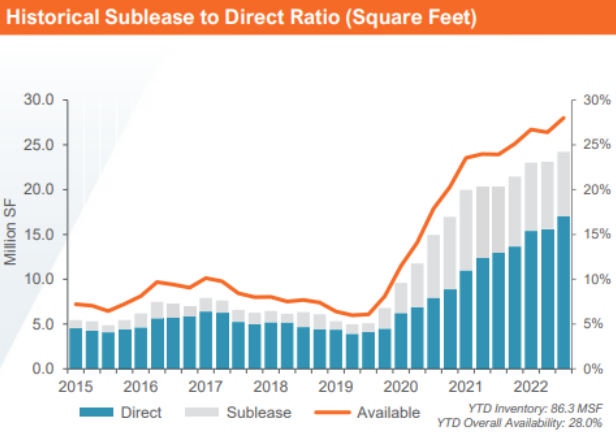

The San Francisco office market consists of 86.3M sf. Presently 28% of the market is available for lease, including both direct space and sublease space, for a total of just over 24M sf. We’re on pace to finish the year with available supply of 30%. The trend in demand (downsizing) and the near certainty of continued macro-economic headwinds in 2023 make it likely we’ll add another 3% to 5% to available supply by the end of ‘23, bringing total availability as high as 35%. It’s too early to predict what 2024 will bring (hopefully a hockey stick graph showing increased demand for office space), but we believe it’s quite possible we’ll see available supply at or near 40%.

We want to talk about this because 30% to 40% available supply is a staggering amount of space (40% is 34M sf). Under normal market circumstances available supply fluctuates (at least partially) due to the introduction of new buildings. These days, supply is increasing exclusively as a byproduct of reduced demand, not new buildings. Positive net absorption is when the amount of available supply is reduced from one period to the next (e.g., quarter to quarter or year over year). Since 2020 we’ve had large amounts of negative net absorption, including this year and very likely next. A healthy market, one in a state of equilibrium, has available supply of around 10%. From 2012 through 2019, net absorption averaged 1,364,942 sf per year. During this period, we had a low of (347,970) in 2017 due to supply additions and a high of 4,838,667 in 2018, the apex of demand during the last cycle. A year in which we achieve 2M sf of positive net absorption in San Francisco would be above average. Consider that it would take 12.5 such years to lower market availability from 40% to 10% (e.g., to absorb 25M sf). What does this mean? It means the impact of all that’s happening now will have a long tail, a period during which despite improvements in the economy and increased demand for San Francisco office space, the volume of available supply will result in a prolonged period of market softness.

For some owners there simply won’t be a pathway to successfully navigate this market and survive to fight another day. And even as buildings trade at much lower valuations, some percentage of supply will remain unleasable as limited demand will naturally gravitate to the best product first. This is when the asset conversion discussion will accelerate. But this, too, is a tricky dynamic because the same problem that’s causing so much supply in the office market (e.g., lack of people coming downtown to occupy office buildings) is also making it less desirable to live downtown, plus it’s expensive to convert product type and not all buildings lend themselves to such conversion (not to mention the backdrop of a declining housing market).

With so much at stake in both the public and private context, it’s important for stakeholders (building owners and government) to take a sober view of potential market performance in the coming years. We appreciate a hopeful outlook as much as the next person, but it’s time to start aggressively planning for more dire outcomes (you know that old saying, “hope for the best and prepare for the worst”). After all, we’ve got enough data now to acknowledge several facts. Firstly, we know there is a reset underway in terms of where knowledge-based workers work. Corporate sentiment about remote work will continue to fluctuate, but hybrid work is here to stay and the continued adjustment by occupiers to hybrid workplace solutions will result in less demand for office space. Adding to the workplace reset, we’re also experiencing a broad repricing of assets, including of company valuations both public and private. Now that capital is expensive and difficult to acquire, companies are no longer focused on the growth at any cost approach. The new objective is profit. This transition requires cost reduction which often begins with the 2 largest expenses: people and real estate. This means less office space.

Market participants can’t “hope” their way through this. For owners of all but the most premium office assets, success will require swift and decisive action to get ahead of rapidly declining market fundamentals by pricing available supply correctly and spending at the asset level to create best-in-class amenities. We personally believe the most successful owners will also establish a variety of ways in which demand can engage with their asset, from traditional leasing, to coworking to flex leasing. City leaders must do all they can to prepare for a long winter of declining tax revenues and increased challenges in promoting and supporting downtown San Francisco. This means spending on the right initiatives to ensure a safe and attractive downtown, while working closely with investors to cut through red tape and support all manner of creative solutions. It’s going to take the entire community, leaders from both business and government, working closely together to navigate this time of significant change.

There is something different on the other side of this. We continue to be hopeful we’ll emerge from this period of change with a new, more vital downtown marketplace. How so? Well, for starters, downtown may become less office-centric, a more holistic place with buildings that serve as hubs for residential, work and retail activities. Green space might become more prevalent as transportation patterns change with more people walking and cycling. Indeed San Francisco’s future downtown has a chance to become a more compelling place, one that accentuates the natural beauty of the surrounding hills and bay while supporting a more diverse spectrum of life and work. It’s way easier to simply hope that things will revert to the way they were in 2019. But the evidence strongly suggests this won’t happen. We’ll all be better off if we begin to focus the collective genius of this great region on defining what’s next.