2021 Archives

TenantSee Weekly

Connecting Fees to Services: Identifying the Best Tenant Advisor

The tenant advisory business was built on the premise that the advisor holds essential knowledge about where your office should be located and how to negotiate market-favorable lease terms. Yet much of the details surrounding what the advisor knows, how they know it and why they advocate a specific strategy are unknown to the client. Importantly, in the US, the advisor’s compensation is often misunderstood by the client since the advisor is paid by the landlord (the tenant actually pays the fee through rent). In fact, with tenant advisory fees being “at risk”, meaning they are earned only if a transaction is completed, there is ample incentive for tenant advisors to hold a strong bias toward transacting quickly, even when it may not be in the client’s best interest. Further, when the service offering is mostly opaque, the provider can increase the value of fees by limiting the amount of service required for their acquisition. This is not a cynical view of the sector. It is a reality based discussion of the structural challenges that make hiring the best advisor difficult.

Understanding this structural market risk, occupiers can begin to align advisor compensation with services. At this point, key differences will emerge between advisors. Best in class advisors will embrace the dialogue. They want transparency because they know they’ve built a service model that creates more value for the client and stands in stark contrast to advisory services centered on space finding. As occupiers become more skilled at connecting fee to service, the competitive pressure will improve the overall marketplace. This is particularly important now, as occupiers embark on a new normal in terms of how they think about office space (vehicles to promote employee engagement), one that requires more from their advisory partners.

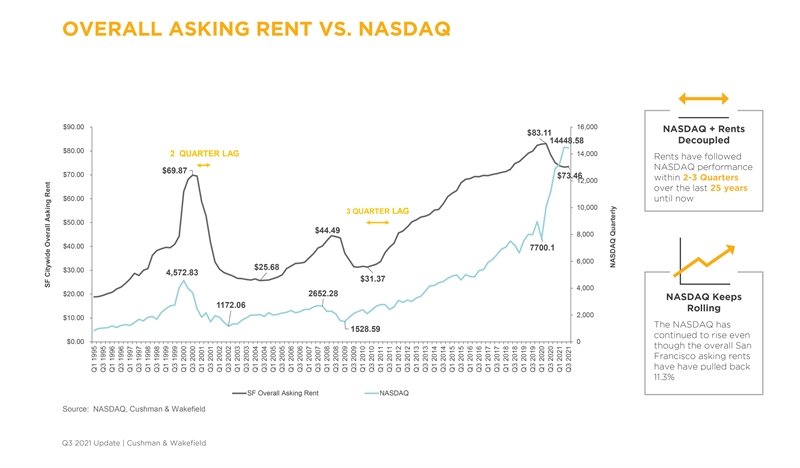

Nasdaq vs. San Francisco Office Rents: Uncorrelated

Way back in 1995 we began tracking the correlation between San Francisco office rents and the Nasdaq. This has become a throw away datapoint since it rarely reveals anything new. That is until Q2 2020. This is when, for the first time in a quarter century, the Nasdaq and San Francisco rents have become uncorrelated. What does it mean?

In simple terms, it means that many tech companies have continued to perform well through the pandemic, despite decreasing the amount of office space they occupy (resulting in more vacancy and lower rents). To be sure, the tech sector is not done with the office. Look no further than Meta’s recent leasing of 1.2M sf of Bay Area office space. These companies will continue to hire and need space to house their employees. But will they also continue to advocate strategies that enable a portion of their employees to work from anywhere? If so, this may make it harder for landlords to chip away at high vacancy levels coming out of the pandemic. Overall, landlords should cheer, not fear these lines crossing. After all, an underlying tech economy that is performing well, albeit while its participants are occupying less office space, is far more favorable than the alternative which can best be illustrated by what happened in San Francisco in 2001, when the underlying economy took a nose dive. Then rents fell off a cliff. This is why rents have held relatively firm through the pandemic, thus far. But it’s also true the as leases expire and companies look to reset on their space needs, vacancy may remain stubbornly high.

The big disconnect is an economy that is performing without the office. Our view of San Francisco is there will be a period of time over the next 24-36 months while occupiers can assert considerable leverage in solving for their office needs, but at some point toward the end of that window, as the pandemic has moved into the rearview mirror, the pendulum will swing more toward being in office and the presence of a healthy economy will, once again, begin to shift the market dynamic away from occupiers.

Why Do We Have Offices

This is the question every company should be asking before it establishes a formal plan for returning to the office. How does office space serve the company and its employees? Many years ago, when the first offices were built, they reflected the factories of the Industrial Revolution. Employers needed to bring employees together to facilitate and monitor their work. Today technology allows people to work productively from anywhere. But for special purpose spaces (e.g., lab space), companies and employees don’t need office space to do their work. So the office has long since stopped serving its original purpose. But there are other reasons for its existence.

Among the relevant considerations are net income (productivity), employee health and happiness and cultural values. The only way to understand how having an office vs. not having an office translates in terms of these variables is by comparison and solving (to the best of your ability) for extraneous factors that otherwise influence outcomes. It’s difficult but that doesn’t mean you shouldn’t do it. For example, with many companies having operated mostly out of office for at least 18 months now, it’s reasonable to compare how the business has performed during this period vs. the same period pre-pandemic. This comparison will obviously be flawed, if, for example, you’re in the office leasing business like we are here at Cushman & Wakefield. For us the pandemic has had an outsized impact on our business such that we can’t reasonably compare the effect of being in or out of the office on net income. The presence of abnormal factors that make one period a poor reflection of the norm render the comparison meaningless. But for many companies, no such abnormality exists, making it reasonable for the change in office use to be studied as an influential variable impacting net income. Did net income increase, decrease or stay about the same? If it increased or was equal, it’s possible the firm can perform equally well or better without an office (in the context of net income). Yet there’s other factors that matter a lot, too. How does having an office vs. not having an office impact employee health and happiness? Maybe the employees are productive but perhaps they’re at greater risk of burnout working from home because they’re working too much? And we can’t forget about culture. Culture is really a measure of stickiness, or employee loyalty. The effect of bad culture is a lack of loyalty and higher employee churn, which can be very expensive. Next to compensation, culture is the biggest variable impacting whether employees stay or go. So it’s reasonable to compare the employee’s views on culture pre-pandemic when they were mostly in the office, to now when they’re mostly of out of the office.

All of this can be discovered through carefully crafted surveys that ask the right questions. It’s likely that most companies will come away with an understanding they need to change how they define and create their offices in order to better meet the relevant goals of increasing productivity, make their employees healthier and happier and building strong culture. At this point, design professionals can help realize the fulfillment of these objectives through space design.

Risk vs. Reward in a Shifting Market

When tenant and landlord negotiate to extend a lease, each party must manage a distinct risk/reward calculus against the backdrop of the market. But irrespective of market, a successful negotiation will always hinge, in part, on identification and exercise of leverage. Of course, this is easier when the market is skewed heavily in favor of one of the participants. To be sure, there’s a lot more to success than just maximizing leverage. Yet now, when the market has undergone a material shift, it’s a good time to ponder the risk/reward relationship.

Over the years I’ve seen some ugly miscalculations. Sometimes these failures are due to what I would characterize as “circumstances beyond the negotiator’s control”. We have to always remember negotiations are done by people. People have bosses, investors, lenders, partners and others who influence their bidding. Here, I’m writing about the failure caused by ignorance or hubris.

How do we avoid such failures? We must be curious, educated and disciplined. Among the key roles of a real estate advisor is to provide perspective and knowledge. Transactions must be understood in terms of their impact on both parties. Each party has options (most of the time). Know your own, yes, but also know theirs. What can they accomplish if they don’t make the transaction on your terms. This is how we come to understand the inflection point at which risk outpaces reward – the danger zone.

When market leverage shifts in a material way, the party whom has enjoyed outsized leverage is often ill-prepared to meet the demands of the new market reality. They’ve become lazy, having named their price for so long. They make mistakes, they miscalculate. This is the environment in which we find ourselves today in San Francisco. The extent to which people adapt quickly and embrace the market, such as it is, will be a deciding factor in separating the early winners from the losers. Sure, if you can afford to eat vacancy for long periods of time, you could simply do nothing (e.g., not lease space) and wait for a better day. But very few landlords are in a position to do so; and, even if they were, it’s unlikely to yield better results. Landlords who are well-advised, curious and knowledge seeking, will, more often than not, find ways to keep their tenants. In a market where available space is likely to remain high over the next few years, vacancy quickly shifts from opportunity to liability. For the tenant, it’s about knowing (and respecting) the point of indifference. Understanding when the negotiation has reached a place where the counter party is reasonably assured of the same or better outcome if you leave. Since you’ve likely dragged them there, kicking and screaming, understand that they may be looking for a reason to walk away. So while tenants will (mostly) enjoy more leverage over the coming years, this is, nonetheless, a time to manage risk and reward with care.

Mo Data Mo Better

There’s not a single decision we make that isn’t improved by access to more data. The challenge lies in gaining access to data, in prioritizing which data matters and in drawing appropriate insights from the data. For many years the business of tenant advisory involved an opaque transaction between a broker, whom had access to data, and a customer, whom did not. Given that tenant advisors are mostly paid by the landlord counter party, the connectivity between scope of services and fee is muted. This has resulted in the tenant advisory industry being built largely around 2 services, 1) site selection and 2) negotiation of basic business terms (rental economics). These services are easy to stand up and difficult for the customer to measure. Over the past couple of decades, the model has improved; but, frankly, the level of services provided to the tenant customer (in many cases) remains low. Certainly large corporate occupiers benefit from the best service platforms brokerages have to offer. But for medium and smaller companies (5,000 employees and less) there remains substantial room for improvement. Not surprisingly, technology is beginning to play a key role in changing the quality of services being offered by many brokerage advisory firms.

Way back in 1987 a group of individuals had the vision to build a company around the thesis that aggregating commercial real estate data would be valuable to the CRE industry. Today, Costar, is the world’s largest aggregator of commercial real estate data and it has a market cap of ~$33B, larger than all of the world's largest real estate service firms but one, CBRE at ~$35B. In fact, Costar is valued more than the next 4 largest publicly traded service firms combined (JLL, C&W, Colliers, Newmark). This clearly illustrates the value of having access to large amounts of data. Not convinced? Consider that Costar does not provide advisory services – it is not a brokerage business. Without brokers feeding it data for free, it would have none. Yet brokers pay large sums to gain access to Costar’s products. It aggregates the data, facilitates easier and better analysis of the data and presents it all in a visually intuitive format. It’s like Zillow for commercial real estate; or, perhaps more appropriately, Zillow is like Costar for residential real estate. But I digress. Access comes in many forms. Fundamentally, a tenant advisor’s service is improved by using Costar, which is why the business is so valuable. But Costar is just one example of a resource that is changing the industry. Good tenant advisory is also well served by access to a robust landlord advisory and capital market advisory businesses. In fact, the more information to which a tenant advisor has access, the better it can advise its clients. Why? Because successful tenant advisory requires much more than access to supply data. It’s important to know the state of tenant demand and the historical transaction values being achieved in a given building and market. Capital market intelligence, knowing the debt and equity stack, for example, and the investor motivation, is invaluable in developing a winning negotiation strategy. The “Achilles heel” of firms that only do tenant advisory is they lack access to critical data that is otherwise essential to quality tenant advisory. They (cleverly) distract from this inadequacy by attempting to shift the dialogue toward conflict, claiming they can advise the tenant better because their firm does not advise landlords and therefore is “conflict free”. What we know is that scale is a good proxy for access to data. The larger the firm, the more engaged it is in the market, the more data it creates and collects and the better it can serve the client.

But access, alone, is not sufficient to create optimal outcomes. Occupiers must understand what data is most important in shaping the best solutions for their specific needs. Some advisors have resources and services that help tenant customers define key drivers affecting occupancy. This prioritization is what shifts solutions from low value “space finding” to high value creation of custom employee experiences that drive engagement and productivity. The market-leading example of this is Cushman & Wakefield’s Experience per Square Foot consultancy.

Finally, there is the question of insight. Insights are gained through disciplined analysis of data consistently practiced over time. Only the largest firms are able to offer such insights. Firms like Cushman & Wakefield have massive research teams spread across the globe. These teams are designed to interface with market experts on the ground in local markets in order to gather, organize and analyze the data derived from their market engagement. I’m not talking about the stale recitation of stats from the prior quarter. I’m referring to forecasting, identification of trends and perspectives that help occupiers think intelligently about the future.

Perhaps most importantly, the brokerage industry is (finally) beginning to use technology to deliver more transparent and intelligent customer service offerings. Tech like Cushman & Wakefield’s TenantSee, a platform which combines the essential elements of a full-scope service in one place to create a more intuitive, informed client experience, is literally changing the way customers experience our industry. These solutions bring transparency to both the data and the process, allowing for more robust client participation. This is the future of tenant advisory; a place in which the customer engages its advisor for transparent presentation of critical data, for consulting to prioritize which data matters and for experts who can provide meaningful insights, driving strategy and value creation.

"It's Not You...": Matchmaking in the Modern Office Market

Is there an underlying science behind which occupiers are attracted to which buildings? Kind of like the effect of pheromones in human sexuality? Maybe.

Office demand can be categorized into 4 basic buckets (“Occupier Demand Categories”):

1. Premium FIRE (Financial, Insurance and Real Estate)

2. Commodity FIRE

3. Big Tech

4. Emerging Tech

The characteristics which define how each Occupier Demand Category evaluates office buildings can be translated into something we call an Experience Score; an overall measure capturing the interplay of a wide range of variables. These variables are broken into four groupings, each of which has a number of sub-variables:

1. Flexibility

2. Image

3. Health & Safety

4. Accessibility

Distinct Occupier Demand Categories place more or less value on each variable leading to a unique Experience Score. Why would any of this matter? Well, for starters, assessing market options through the filter of Experience Scores can help isolate the buildings that best match your particular demand. Potential fit can be evaluated on the basis of how well a building’s Experience Score is correlated with your Demand Category Experience Score. The higher the correlation, the better the match.

Creating the right office solution requires prioritization of and navigation through a complex web of drivers. It’s not merely about location and cost. It’s about the total experience you create for your employees. Experience Scoring leads to better site selection; and, ultimately to better workplaces. Contact us to learn more.

Who's On First

Dating myself with an Abbot and Costello reference. But the unnecessary confusion so many companies experience when trying to prioritize key factors that influence their real estate decisions reminds me of that famous skit.

Finance, HR and Workplace. They don’t always communicate so well together. Our view is that Workplace should be the place in which Finance and HR sing together in perfect harmony. A successful workplace is the result of proper alignment between the two. Most companies aren’t in the envious position of viewing workplace entirely through the lens of what’s best for employees (e.g., HR). Cost constraints are a real thing. However, it’s also true that myopic focus on cost will (mostly) result in a failure to properly address key employee drivers. After all, one of the most important reasons for having an office is to enhance employee experience and productivity – a tangible way in which companies can make themselves more attractive to key talent. And Workplace should never be out ahead of Finance and HR, acting independent of either. Yet, too often, we see companies struggling to understand and prioritize the key drivers that define what their office should be.

We’ve long advocated something we call a “Create – Get” approach to office solutions. What does this mean? It simply means that companies must first create their optimal office solution before going to the market to get it. Unfortunately, real estate processes often begin at “get”, as in, “…let’s go get some office space”. As we navigate our way out of the pandemic, with renewed focus on the value of the office (it’s about employees), it’s more important than ever for companies to step back and align the interests of Finance and HR to ensure they are maximizing the value of the custom employee experiences they create.

Rental Rate: A Poor Proxy for Value

Historically, rental rates have played an out-sized role in determining where companies lease office space. Today, as companies address leases they negotiated in 2010 – 2015, they understandably do so against the backdrop of the pandemic. The fact that many companies have not yet fully returned to their offices has created a sense among occupiers that rental rates should be substantially lower (e.g., the office market must be very soft since no one is there). But paying for space and using space are 2 different things – landlord rent collections remain high (~98%). San Francisco rents are down. But as of Q3, citywide average rents stand at $73.46, down only 12.4% from the pre-pandemic high; and class A CBD asking rents are $84.91, down just 7.4%. Hence, in most cases, tenants having leases expiring in 2022 and 2023 will find their rent is actually increasing from the in-place rate. This gap between expected outcomes and market reality can sometimes cause occupiers to make poor decisions. Rate, alone, is not a good measure. Total occupancy cost per employee is better. But the real question is what do you get for the cost? How does the occupancy cost impact the following:

Promotion of employee health and wellness (outdoor space, air quality, natural light, fitness, etc.)

Flexibility (contraction, expansion, term, etc.)

Design Agility (mobility of furniture systems, change management)

Employee engagement (how well the space promotes engagement)

Recruitment/Retention of key talent

This is not to suggest financial considerations don’t matter. They do. Most companies have budget constraints. But in the context of evaluating which office leasing solutions best serve the company (e.g., the employees), a myopic focus on rent will often lead to the wrong outcome.

So why is rent such a common measure of value? Laziness. The office lease is a complex construct that includes many variables and has broad impact on the company. Assessing and measuring leases on the basis of these broader impacts is harder, requiring a more thoughtful approach. It’s much easier to simply study the cost of option A vs. B. Yet even with respect to cost, there is way more to consider than rent. Space design and construction, for example, can lead to vastly different capital spending from one space to the next.

Before the pandemic, office tenants were beginning to evaluate space more from the perspective of employee impact (largely led by the tech sector). But the pandemic has accelerated this trend. If your company is still making leasing decision based purely on rental rate, it’s time to change the conversation. Your best competitors have already embraced the connection between employee engagement and space and are focused on creating optimal employee experiences through the spaces they provide. These companies will leverage their offices to attract key talent and strengthen their competitive advantage.

Market What?

One key feature of the tenant advisory platform my partners and I created, TenantSee, is the Market Diagnostic. What is it? In short, it’s an output we provide our clients, at no cost (it’s part of our advisory platform), which draws from a spectrum of subject matter experts within C&W to develop a narrative regarding leverage in a specific asset, in a specific market. It incorporates knowledge from our capital market and debt teams to understand an owner’s debt and equity positions. We engage our asset teams to identify operational variables relating to the asset. We leverage our research group for data regarding lease roll (Landlord exposure) and completed transactions in the asset and the comparable market. We study the owner’s motivation profile. In total, we develop a comprehensive market leverage narrative for our client that is sensitive to the asset, the market and timing. Included in our deliverable is an indifference analysis, in which we clarify the value of a heavily discounted in-place lease extension vs. a “market” lease value (what a 3rd party tenant would be willing to pay for the space) in order to show the value at which the owner is otherwise indifferent whether our client renews or vacates. This is vital information as we think about the economics of the existing building. We also assess our client’s comparative cost of staying vs. relocating to several comparable buildings, including year one capital spend. In totality, this gives our client great market insight, months before it needs to engage in a market process. In other words, the Market Diagnostic is a resource we provide to help the client begin thinking (correctly) about a market, given the variety of market-based drivers impacting outcome.

Of course, the most critical drivers are those defining the client’s need for space. And we know those drivers don’t necessarily synch with lease timing. This is why we typically begin providing Market Diagnostics 3 years prior to lease expiration, with updates every 6 months thereafter. Not surprisingly, we often discover there is a sweet spot between market and client dynamic that calls for beneficial action ahead of an expiring lease.

Providing a Market Diagnostic is the single easiest way for us to demonstrate how we think about tenant advisory. We often do so on a complimentary basis, in order to explore our potential fit with prospective clients. Regardless of the outcome, the Market Diagnostic provides a trove of valuable insights. If you’d like to learn more, or maybe have us assess a market for your company, please reach out.

When 1 = 1.25: How Your Office Building Continues to Grow

A 10,000 sf office space is not actually 10,000 sf. In a high-rise building in downtown San Francisco, the “usable” square footage in a space having 10,000 rentable square feet is likely closer to 8,000 sf. But the tenant pays rent on the basis of 10,000 rentable square feet. Why is the tenant charged rent on 25% more space than it can actually use?

A 10,000 sf office space is not actually 10,000 sf. In a high-rise building in downtown San Francisco, the “usable” square footage in a space having 10,000 rentable square feet is likely closer to 8,000 sf. But the tenant pays rent on the basis of 10,000 rentable square feet. Why is the tenant charged rent on 25% more space than it can actually use?

The answer lies in the measurement methodology used to measure large scale office buildings in major US markets. This methodology was developed in 1915 by an organization, founded in 1907, called BOMA. BOMA stands for Building Owners and Managers Association. BOMA’s standard of measurement gets a periodic refresh. I have never seen one of these refreshes result in a reduction in building size…it’s always the opposite. This is why, upon renewing a lease, tenants sometimes find the landlord has remeasured the space and it is now larger than it was the day immediately preceding the measurement; and, the difference isn’t due to having made a mistake with the original measurement. It simply grew.

Usable square feet are square feet you can actually use. Rentable square feet is a made up concept. The difference between rentable and usable square feet, often referred to as the “load factor” includes things like a percentage share of “off-floor mechanical systems” and a share of the building’s lobby and the common areas on a multi-tenant floor. In other words, it’s a way for the building owner to charge rent on portions of the building that are not otherwise directly leasable to the tenant(s). The argument, of course, being that all tenants benefit from these areas (lobby, mechanical rooms, etc.).

Adding to the confusion around how buildings are measured is the fact that, notwithstanding the standards, owners often take “liberties” with how the measurement is conducted. You will know this is the case when the owner describes its building as being measured “…in accordance with a modified BOMA standard”. Hmmm. Modified how? By the way, let’s not forget, we’re already starting from the perspective of building “owners and managers”. This is not the “building occupiers” measurement methodology. There’s an old real estate joke about the floors in New York City buildings being measured to the center of the street.

One thing that keeps building measurement in check is market competition. When a building is poorly designed and/or an owner takes too much liberty with the measurement, the inefficiency is revealed in the form of higher cost/usable square foot – a comparison tenants should always make when studying multiple buildings.

Why Institutional Investment Keeps Rents High

When I began my real estate career in San Francisco in the early 1990s, office buildings were mostly owned by private investors using a relatively small selection of institutional capital partners. The Shorenstein Company, whom I worked for from 1990 – 1995, was a great example. At that time, they were the largest owner of office buildings in San Francisco, holding 11M sf. During those days, most owners, including Shorenstein, employed a simple strategy centered on preserving tenants while minimizing cash requirements (funding of tenant improvements, etc.). In most cases, the first choice was to keep the existing tenant by offering a rental rate which was discounted to market. If that failed and the tenant moved out, the next step was to undercut the market by lowering the rental rate to steal a tenant away from another building. The goal was to buy and manage the asset to generate maximum cash flow, which the investors counted on each quarter. Importantly, the majority of assets were owned by this type of investor. But by the mid-1990s, the nature of office ownership was beginning a period of significant change which would materially impact rental economics for decades to come.

There were 2 main catalysts for this change. First, the resurgence in real estate investment trusts (“REITS”), a form of ownership that was developed in 1960 but which really didn’t gain traction in US office markets until the mid-1990s. Second, in the 1990s, asset allocation theory began calling for institutions to increase their share of real estate holdings. These two events resulted in a wholesale shift in the type of ownership structures dominating markets like San Francisco.

Today, office ownership is mostly institutional, with very few owners playing by the “old” playbook of cash flow preservation. Nearly all the institutional owners subscribe to a similar strategy, one that is geared toward maximizing future asset valuation for a sale. To perfect this approach, an owner may not want to keep an existing tenant whom is seeking to renew its lease at a discount to market, because despite the cash flow benefits, the associated negative impact on asset valuation is counter to investor objectives (e.g., future profit from sale of the asset). There are many “buckets” within the category of institutional investor. Yet the primary focus is always on asset valuation, causing these owners to behave in unison. Rental rate is no longer the main form of competition. Instead, owners compete with concessions and amenities. Things like tenant improvement allowance, free rent and cash allowances to offset rent; and, luxury project amenities like fitness facilities and tenant lounge space. Lowering the rental rate is a lever of last resort. This has had the aggregate effect of holding rates higher even as the markets face mounting pressure.

My Landlord Offered Cash To Offset My Rent...Why?

Landlords seeking to preserve future sale value have to protect the rental rate. The future sale value is tied to the building’s net operating income (“NOI”). NOI is the value achieved by deducting operating expenses and taxes from gross rent. This value is then capitalized using a cap rate to determine asset value. Hence the higher the face value of the rental rate, the greater the NOI and the higher the asset value.

This is why institutional landlords will often load up a lease transaction with concessions while holding firm on the lease rate. The 2 most common concessions are free rent and tenant improvement allowance. Free rent is self-explanatory, it is a period of time during which the tenant is not obligated to pay rent. But the use of tenant improvement allowances with a rent offset feature is a relatively new approach in the San Francisco market. Here, the landlord provides an up-front cash allowance which the tenant can then use to offset rent. This is why, even when a tenant may not require any additional tenant improvement work, it may find that its landlord is offering a tenant improvement allowance. In contrast, owners that employ a long term hold strategy which emphasizes cash flow preservation and limited ongoing capital spending will simply lower the rent as needed to keep the tenant. They’re not as concerned with future asset value.

Under GAAP, most tenants account for the annual lease cost as the straight line value of the total projected expense. Landlord allowances used to offset rent and free rent would be amortized over the term and deducted from the rent expense value. In theory, under GAAP, the tenant should be indifferent to 1) an $80/sf start rent with 3% annual increase over a 7 year term where the landlord is also providing 12 months of free rent and a $30/sf TI allowance which can be converted to rent AND 2) a transaction in which it pays $71.85/sf flat for the 7 year term. Of course, the difference is cash. The former scenario, requiring no cash in the first 16.5 months of the term, escalates to a year seven cost of $95.52/sf, requiring substantially more cash than the flat $71.85/sf cost. When contemplating leasing scenarios that provide significant front end discounts but reflect a high start rent, it’s important to model the future leasing expense and rationalize this cost in the context of annual operating budgets.

A Level Playing Field

This week we’re writing about an old topic that surfaces every now and again, usually when we come across a tenant who has chosen to negotiate a lease or lease renewal on its own. Why would a tenant do so? I think the most common reason is perceived savings. This scenario seems to play out most often in buildings owned by private investors (e.g., not institutions). Buildings where the landlord calls the tenant directly and proposes to renew the lease at a discount if the tenant negotiates without a broker.

But how does this work, in practice? Let’s say the tenant leases 10,000 sf and is contemplating a 5 year extension of the term. The broker fee would be $100,000. So in order for the landlord’s contention that it will credit the fee back to the tenant for negotiating without a broker, the ultimate transaction value has to be $100,000 less than the value otherwise achieved via an arms’ length negotiation. So how can the tenant quantify this value? Was it given in the form of a $2/sf/year discount to the “market” rental rate? Is it an additional $10/sf in landlord funded tenant improvements, above the market amount? Is it $100,000 more in free rent? Perhaps most importantly, how can the unrepresented tenant know the fully leveraged market value; or, how can it know what the landlord would be willing to accept in a fully leveraged negotiation?

Whenever I hear that a tenant chose to renew its lease without a broker, I don’t think of savings, I think of cost. How much more did the tenant end up paying for this lapse in judgment? The fact this still happens is indicative of how poorly tenant advisors communicate their value. For a 10,000 sf space priced at the market average ($72/sf), the leasing fee represents <3% of the total transaction value. Even a mediocre broker will create at least 10% in cost savings. That’s a layup. Even if you pay your advisor directly, you’ll come out ahead by doing so.

Take the time to talk with a few brokers to understand how they collect market data, what their data shows about the current and projected market environment; and, how they create and utilize leverage to decrease cost. Ask them how the value they create correlates with the fee they earn. Finally, consider that landlords are in the real estate business every day. It’s their business to know the exact value of their asset and to do everything possible to increase that value for their investors. They come to the negotiation armed with knowledge. Good tenant advisory, among other things, levels the playing field and permits tenants to access fully leveraged (discounted) values.

Less Space, More Uncertainty

Over the past year our small team based in San Francisco has not worked on a single assignment in which the client is expanding its leased office space. In some cases, the leased footprint remains the same, but many clients are decreasing their leased space. We're doing work all over North America. Client approaches to the office range from the following:

1. Wait and see: Not really using their space, mostly work from home and not willing to take a long term position on the market. In some cases letting the lease expire without solving for a new space.

2. Hybrid: This is by far the most common approach. It can be very studied, the result of a thorough workplace strategy; or, it is often an approximation based on a guess of how many employees will choose to work remotely some of the time going forward.

3. Full Remote: This is a much smaller percentage.

4. Fully In Office: This is also a smaller percentage.

While there’s a lot of uncertainty, if our comparatively small business reflects the broader trend, it portends a net reduction in office demand over the next several years. Of course, the big variables influencing this include how well the virus is managed in the future (e.g., efficacy of vaccines against variants) and employer/employee expectations and behavior. On this latter point, change is inevitable. The nuance lies in how the employer/employee relationship evolves once the virus is under control and companies look to modify workplace expectations. Despite the small percentage of companies that are opting to work fully remote, most continue to believe in the importance of having employees come to the office. But after ~2 years of adjusting to work from anywhere, maybe the employees will have other ideas?

The only bet that seems certain, in the near term, is that office supply will remain abnormally high in many US Metro markets and urban core retail will suffer due to reduced daily populations. From the office occupier perspective, this unique market dynamic will create select opportunities to secure longer term cost savings. But few companies may be in a position to confidently access these opportunities.

We're In A Pandemic, Why Is My Rent Increasing?

This is a common question for tenants looking to negotiate lease extensions in the current market environment. Intuitively, they expect their occupancy cost to decrease due to the effects of the pandemic (e.g., higher vacancy, less demand, etc.). However, they often fail to realize the point of impact, or the base values on which market softness has its affect, are values that were in place just prior to the pandemic, not values from 5+ years ago when they signed the original lease. Most importantly, over the course of their lease, rents in the San Francisco office market appreciated 50% to 75%. By way of example, let’s say a tenant executed a lease 7 years ago at a base value of $53/sf. Over the course of the lease, the market for their space appreciated 65%, reaching a high of ~$87.50 (this would have been January of 2020). When the pandemic hit the market decline began at $87.50, not $53. Today direct asking rents are off about 12%. So the current market value for this space is in the upper $70s; whereas the tenant’s rent, after annual increases, is likely in the mid $60s. Adding to this is the fact that in San Francisco, direct availability (not sublease) is about 10%. This is why direct lease rates are only off about 12%. Sublease space accounts for 45% of available supply. These 2 markets (sublease vs. direct) perform differently as the parties have significantly different motivations. The sublandlord is looking to mitigate cost as quickly as possible and the landlord is looking to preserve or enhance asset value.

Skin In The Game

In his book by the same title, Nassim Nicholas Taleb writes about the “hidden asymmetries in daily life”. In Chapter One, Taleb writes, “Beware of the person who gives advice, telling you that a certain action on your part is “good for you” while it is also good for him, while the harm to you doesn’t directly affect him”. Taleb’s book makes me think about the business of tenant advisory. I can’t think of a business that fits more squarely into this narrative, especially here in the US where tenant advisors are paid by the landlord, not the tenant they advise. There are so many aspects of the advisor/client relationship that are opaque. In many markets, the common practice is for the advisory fees to be “per separate agreement”, meaning the client isn’t even aware of how much the advisor is being paid. The company hiring the advisor has been subjected to a long standing market practice which causes it to believe that so long as they are hiring an advisor whom appears to have the right credentials and experience and such advisor is agreeing to be paid by the landlord, all is good. But setting aside, for the moment, the matter of how tenant advisors are paid, it would seem, at a minimum, worthwhile for the client to clearly understand how much the advisor is being paid and what services are being provided to earn the fee. It is correct for tenant clients to think about the leasing fee in this way and to hire their advisor based on a clear understanding of which one will provide the most relevant services which are proven to correlate most highly with the achievement of quality outcomes. If the fee were being paid directly by the client, this would be a given. And say nothing of the asymmetries between the amount of fee earned and the terms of the lease. In most cases, these asymmetries are glaring. For example, in some markets, fees are tied to length of term. In others, they are tied to amount of rent paid. So your advisor is paid by the counter party in the negotiation and is often paid more when terms are less favorable to you. This asymmetry has always bothered me. The only solution I’ve been able to find is total transparency such that our fees are always known and that the services we provide are correlated with the fee we earn. I once had a client ask me to negotiate a lease expansion. The market was very tight and the opportunity to extract meaningful leverage from the landlord was slim. To my client’s surprise, I proposed an alternative strategy that would save them millions of dollars over the “captive” expansion. They were grateful but insisted they wanted to proceed. There wasn’t much to be done. The fee was 6 figures and it felt poorly aligned with the value we were able to create so I proposed giving a large portion of it back to the client. Their comment was they understood the risk associated with my business, they realized that much of the work I do is speculative (tenant advisors are not paid a salary, only commissions when/if transactions occur), so the fee is appropriate. It is true, there is a high degree of risk in our work. We often work for months (years) on projects for which we are never compensated. But this dynamic only makes the opacity and asymmetry more pronounced, when the advisor’s incentive to close the deal is greater than its incentive to maximize client value. Fortunately there are many excellent tenant advisors that rise above the structural challenges of our business to provide truly valuable services, to earn their fee. Maybe there are similar asymmetries in your business? I highly recommend Taleb’s thought provoking book.

A Short Discussion of Operating Expenses and Taxes (Insert Big Yawn Here)

I know. This is painful. But you need to understand it, so here goes. A third or more of a tenant’s occupancy cost is attributed to the operation and taxation of the building in which it leases space. Yet these costs and how they are distributed are often a source of confusion.

Firstly, there are several ways in which landlords deal with these expenses. In San Francisco, for most class A buildings, the common approach is what is known as a full-service, gross lease with a Base Year. In this case, the Base Year is established during the negotiations, typically the year in which the new lease commences; provided, however, if the lease starts in the 2nd half of the year, the Base Year is often pushed to the following calendar year. In simple terms, during the Base Year, the tenant pays only its Base Rent. So, for example, if the Base Rent is $70/sf, it only pays $70/sf. The total amount of operating expenses and real estate taxes for the full calendar year, less any excluded items, is then established as the Base Year amount. For example, if the operating expenses total $18/sf and the taxes are $5/sf, the total Base Year value is $23/sf. The tenant then pays its pro rata share of any increases above these amounts as such increases may occur in subsequent lease years. So if operating expenses go from $18/sf to $18.50/sf, the tenant is responsible for the $.50/sf increase. If the tenant occupies 10,000 sf, that translates to $5,000 in additional operating expense costs for that lease year. Similarly, if taxes increase, the value of the increase is passed on to the tenant. Under this lease structure, the building management team will project future increases at the end of a given calendar year and in the next calendar year, charge the tenant the estimated monthly value of the projected increases. At the end of that year, management will “true up” the costs and either bill the tenant for any shortfall or credit back any overage.

Another common approach to leasing is what’s known as a NNN lease. In this lease structure, the tenant pays all operating expenses and taxes. It pays a Base Rent, which is usually lower than the Base Rent you find in a gross lease since the tenant is picking up all the expenses and taxes. So if the space in our prior example was leased as a NNN lease, it would likely have a Base Rent of $47/sf and a total year one NNN rent of $70/sf. The operating expenses and taxes would be the same (e.g., $23/sf) but they would be passed on to the tenant in full from day one. In subsequent years, the cost would increase based on the extent to which the lease calls for Base Rent increases and the extent to which the operating expenses and taxes increase. NNN leases can end up being a little less costly than Gross Leases because the annual Base Rent increases are done from the Base Rent value, not the fully-serviced rent. In the first example, where the starting rent is $70/sf if there is a 3% annual rent escalation, it is calculated off the $70/sf rate; whereas in the case of the NNN lease, the annual rent escalation is calculated off the $47/sf rate.

There are numerous other variations of the concept. For example, some leases are NOE, which stands for Net of Electricity. And there are leases which are NUJ, or Industrial Gross, both of which are net of utilities and janitorial.

It’s no wonder this can be confusing. Adding to the confusion is the negotiation around what should be included and excluded in the calculations. A good real estate advisor will be well-versed in all the different ways in which expenses and taxes are treated and will be able to successfully negotiate appropriate exclusions. This is but one of the seemingly obscure areas in which a tenant seeking to negotiate on its own is likely to miss the opportunity to mitigate costs.

The Math Behind the Motivation

Occupiers often think pricing for office space is one dimensional. Sure, they understand that different quality buildings and spaces translate to different prices. But pricing is actually complex and dynamic, based on many variables, including specific owner motivations. And motivations vary significantly from one owner to the next.

Consider the exact same quality of space in 2 comparable buildings having different owners. On the surface, you might expect the owner’s rental objectives to be similar. However, in practice, they can be drastically different. Why? Because owner motivations and the leverage narrative may be completely different. How can they differ? Start with the asset itself. How much of the building is vacant or soon to be vacant? What percentage of the leases roll in the near-term? What is the owner’s cost basis? Does the owner intend to hold the asset for the long term, or will they look to sell? Is the asset evaluated on a stand alone basis, or is it part of a portfolio? Is the owner a REIT?

It’s not uncommon to see a situation in which one owner is willing to transact for $65/sf; whereas the other won’t transact for anything less than $75/sf. For the existing tenant, seeking to execute a discounted lease extension, the normal approach is to leverage the value it creates by de-risking the owner’s future. Specifically, the extending tenant will often require less capital (tenant improvements) and will not expose the owner to a disruption in cash flow. However, even when the cash flow from the discounted extension of the existing tenant is higher than that from a new deal at full market, the owner whom is focused on max valuation will go for the higher rent, riskier outcome. This is because they’ll make more profit on the sale due to a higher asset value. Commercial office buildings are valued based on the capitalization of net operating income. A $10/sf swing in net operating income at a 5.5% cap rate is worth $181/sf in asset value. If we’re evaluating a 20,000 sf space, that’s worth $3.6M. Even if the owner has to spend $50/sf more in tenant improvements and the space sits vacant for 12 months, the value derived from a future sale is greater than the cost of acquiring the new deal, which is about $2.3M (the additional $50/sf in TI and the 12 months downtime). Further, holding firm on rental value may have an aggregate effect on the values of other space in the asset. So while the owner takes more risk and spends more up front, it comes out $1.3M ahead. Now consider this same calculus over a 600,000 sf asset.

You Cannot Be Serious

Nope. You can’t tell me my space is worth more now than it was pre-COVID. You can’t tell me there’s limited supply. You cannot tell me the market isn’t going to crash. Aren’t we still in the midst of a global pandemic? Didn’t your research team just publish a report indicating vacancy is north of 20%? Aren’t companies cutting back on the amount of space they lease? Aren’t landlords eager to negotiate, at any price, in order to keep their tenants? You can’t tell me we’ve paid rent all through this pandemic even though we’ve barely used our space, and now, when our lease is expiring, we’re facing costs that are comparable to or worse than those we would have faced before this mess ever happened. No way.

The San Francisco office market is highly segmented. What does that mean? It means the type of space you seek to lease will translate to a unique market experience that is distinct from that you would otherwise experience if you were seeking different space. In fact, to enjoy the leverage you would expect in a 20% vacant market, you need to focus on sublease space or so called “commodity” space. Sublease space accounts for 45% of the vacancy. It’s a soft market. Oh, it also comes with term limitations and risks associated with sublandlord default, sublandlord decisions to reoccupy the space and landlord recapture. In other words, it’s usually got some hair on it. Commodity space is the most common space in the market. It’s the space located in the mid-rise and low-rise portions of buildings. It often has limitations on outlooks and natural light. You can access great leverage in both segments. But if you are seeking premium view space, or quality 2nd generation space (especially professional services space), you’re in for a surprise. Pricing is holding relatively firm or trending higher. Why? Because there isn’t much of it. Supply and demand. Market segmentation. Landlords have access to tremendous amounts of data and they can easily slice and dice their availability by segment, enabling them to be more targeted in how they price their space.

So what are the segments? They are:

High-end view space in premium buildings

Sublease space

Short term vs. long term

High quality vs. commodity

Quality pre-built professional services space

Commodity space

If you want to experience the kind of leverage that can be had in a 20% vacant market, go for the segments in which you can access such leverage. If, on the other hand, you are focused on the segments in which leverage is limited, prepare to negotiate like it's 2019.

Maybe It's Time

There’s always been a large gap between what companies need from an office and what the market offers. Over the past decade, as the coworking market rapidly evolved, landlords were forced to rethink customer experience, resulting in an “amenity war” that has made many office buildings more valuable and attractive to occupiers. But despite new lounge spaces, high quality exercise facilities and other project-based amenities, the nature of the office lease commitment in major US metros has remained unchanged. The product is still designed to lock in tenants for the longest possible term at the highest possible price, while minimizing the amount of capital the landlord must spend to win the tenant. Addressing the gap between occupier and landlord objectives may be what’s next in the evolution of the office.

What if a new office product was developed that was pre-built to a high-quality standard and delivered, fully furnished, on flexible terms. A product that functions more like the short-term sublease market (e.g., fully designed, furnished and ready for occupancy). Would occupiers pay more for such an offering? In most US metro markets, a company seeking to lease 5,000 sf of office space will be required to make a minimum 5-year commitment. Yet for many companies, the business will change significantly over 5 years. At $50/sf/year the lease costs $1.25M. The typical tenant will spend an additional $250,000 to furnish and wire the office. What if the same quality space was available on flexible terms? Would it make sense for a company to pay twice as much in annual rent for the flexibility of leasing the space for 1.5 years? Would it be worthwhile for the landlord to make the investment and take the risk of shorter-term occupancies? If you build it, will they come?

To be sure, this model would require investors that are looking to hold over long periods of time and derive their investment returns through ongoing cash flow, as opposed to future sale pricing. Traditional lending formulas would not look favorably upon the model, so leverage may be difficult to achieve (at least until a true market developed for the product). Coworking and landlord-built spec spaces are two ways in which the markets have moved toward creating better solutions. But there are limitations to both. Coworking, for example, generally relies on high-density occupancy of multiple companies in the same space to generate its return. And even though operators have pivoted to “enterprise” models, offering single tenant occupancy, in the end, these solutions behave much like traditional leases. The spec space landlords build is typically designed to appear ready to occupy (in order to gain tenant interest more quickly) but these spaces often require considerable capital investment prior to occupancy. Importantly, landlords still rationalize their capital investment in the space over long-term leasing strategies that don’t deviate from their typical offering. In short, the market has yet to create a product that fully addresses the dynamic needs of the tenant customer. Maybe it’s time?