2021 Archives

TenantSee Weekly

Why Institutional Investment Keeps Rents High

When I began my real estate career in San Francisco in the early 1990s, office buildings were mostly owned by private investors using a relatively small selection of institutional capital partners. The Shorenstein Company, whom I worked for from 1990 – 1995, was a great example. At that time, they were the largest owner of office buildings in San Francisco, holding 11M sf. During those days, most owners, including Shorenstein, employed a simple strategy centered on preserving tenants while minimizing cash requirements (funding of tenant improvements, etc.). In most cases, the first choice was to keep the existing tenant by offering a rental rate which was discounted to market. If that failed and the tenant moved out, the next step was to undercut the market by lowering the rental rate to steal a tenant away from another building. The goal was to buy and manage the asset to generate maximum cash flow, which the investors counted on each quarter. Importantly, the majority of assets were owned by this type of investor. But by the mid-1990s, the nature of office ownership was beginning a period of significant change which would materially impact rental economics for decades to come.

There were 2 main catalysts for this change. First, the resurgence in real estate investment trusts (“REITS”), a form of ownership that was developed in 1960 but which really didn’t gain traction in US office markets until the mid-1990s. Second, in the 1990s, asset allocation theory began calling for institutions to increase their share of real estate holdings. These two events resulted in a wholesale shift in the type of ownership structures dominating markets like San Francisco.

Today, office ownership is mostly institutional, with very few owners playing by the “old” playbook of cash flow preservation. Nearly all the institutional owners subscribe to a similar strategy, one that is geared toward maximizing future asset valuation for a sale. To perfect this approach, an owner may not want to keep an existing tenant whom is seeking to renew its lease at a discount to market, because despite the cash flow benefits, the associated negative impact on asset valuation is counter to investor objectives (e.g., future profit from sale of the asset). There are many “buckets” within the category of institutional investor. Yet the primary focus is always on asset valuation, causing these owners to behave in unison. Rental rate is no longer the main form of competition. Instead, owners compete with concessions and amenities. Things like tenant improvement allowance, free rent and cash allowances to offset rent; and, luxury project amenities like fitness facilities and tenant lounge space. Lowering the rental rate is a lever of last resort. This has had the aggregate effect of holding rates higher even as the markets face mounting pressure.

A Level Playing Field

This week we’re writing about an old topic that surfaces every now and again, usually when we come across a tenant who has chosen to negotiate a lease or lease renewal on its own. Why would a tenant do so? I think the most common reason is perceived savings. This scenario seems to play out most often in buildings owned by private investors (e.g., not institutions). Buildings where the landlord calls the tenant directly and proposes to renew the lease at a discount if the tenant negotiates without a broker.

But how does this work, in practice? Let’s say the tenant leases 10,000 sf and is contemplating a 5 year extension of the term. The broker fee would be $100,000. So in order for the landlord’s contention that it will credit the fee back to the tenant for negotiating without a broker, the ultimate transaction value has to be $100,000 less than the value otherwise achieved via an arms’ length negotiation. So how can the tenant quantify this value? Was it given in the form of a $2/sf/year discount to the “market” rental rate? Is it an additional $10/sf in landlord funded tenant improvements, above the market amount? Is it $100,000 more in free rent? Perhaps most importantly, how can the unrepresented tenant know the fully leveraged market value; or, how can it know what the landlord would be willing to accept in a fully leveraged negotiation?

Whenever I hear that a tenant chose to renew its lease without a broker, I don’t think of savings, I think of cost. How much more did the tenant end up paying for this lapse in judgment? The fact this still happens is indicative of how poorly tenant advisors communicate their value. For a 10,000 sf space priced at the market average ($72/sf), the leasing fee represents <3% of the total transaction value. Even a mediocre broker will create at least 10% in cost savings. That’s a layup. Even if you pay your advisor directly, you’ll come out ahead by doing so.

Take the time to talk with a few brokers to understand how they collect market data, what their data shows about the current and projected market environment; and, how they create and utilize leverage to decrease cost. Ask them how the value they create correlates with the fee they earn. Finally, consider that landlords are in the real estate business every day. It’s their business to know the exact value of their asset and to do everything possible to increase that value for their investors. They come to the negotiation armed with knowledge. Good tenant advisory, among other things, levels the playing field and permits tenants to access fully leveraged (discounted) values.

Less Space, More Uncertainty

Over the past year our small team based in San Francisco has not worked on a single assignment in which the client is expanding its leased office space. In some cases, the leased footprint remains the same, but many clients are decreasing their leased space. We're doing work all over North America. Client approaches to the office range from the following:

1. Wait and see: Not really using their space, mostly work from home and not willing to take a long term position on the market. In some cases letting the lease expire without solving for a new space.

2. Hybrid: This is by far the most common approach. It can be very studied, the result of a thorough workplace strategy; or, it is often an approximation based on a guess of how many employees will choose to work remotely some of the time going forward.

3. Full Remote: This is a much smaller percentage.

4. Fully In Office: This is also a smaller percentage.

While there’s a lot of uncertainty, if our comparatively small business reflects the broader trend, it portends a net reduction in office demand over the next several years. Of course, the big variables influencing this include how well the virus is managed in the future (e.g., efficacy of vaccines against variants) and employer/employee expectations and behavior. On this latter point, change is inevitable. The nuance lies in how the employer/employee relationship evolves once the virus is under control and companies look to modify workplace expectations. Despite the small percentage of companies that are opting to work fully remote, most continue to believe in the importance of having employees come to the office. But after ~2 years of adjusting to work from anywhere, maybe the employees will have other ideas?

The only bet that seems certain, in the near term, is that office supply will remain abnormally high in many US Metro markets and urban core retail will suffer due to reduced daily populations. From the office occupier perspective, this unique market dynamic will create select opportunities to secure longer term cost savings. But few companies may be in a position to confidently access these opportunities.

We're In A Pandemic, Why Is My Rent Increasing?

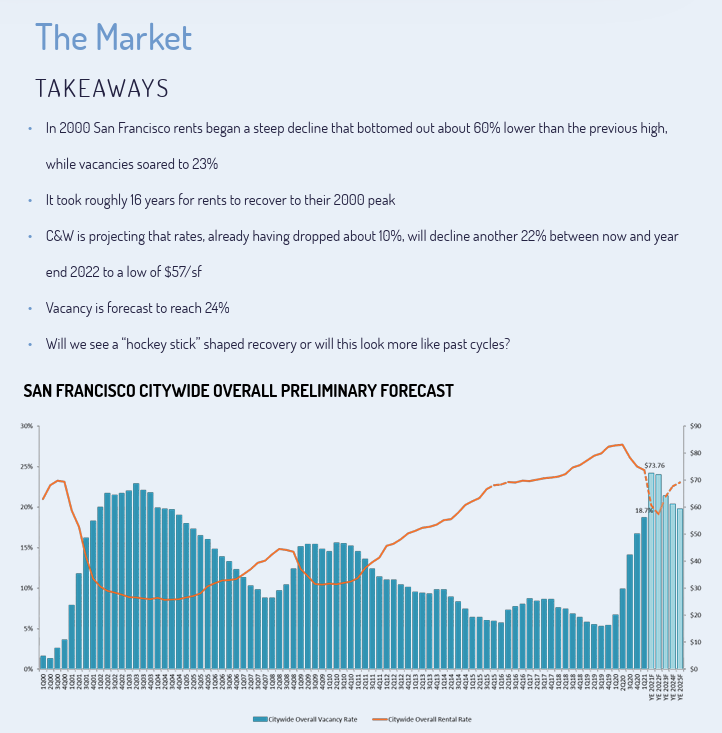

This is a common question for tenants looking to negotiate lease extensions in the current market environment. Intuitively, they expect their occupancy cost to decrease due to the effects of the pandemic (e.g., higher vacancy, less demand, etc.). However, they often fail to realize the point of impact, or the base values on which market softness has its affect, are values that were in place just prior to the pandemic, not values from 5+ years ago when they signed the original lease. Most importantly, over the course of their lease, rents in the San Francisco office market appreciated 50% to 75%. By way of example, let’s say a tenant executed a lease 7 years ago at a base value of $53/sf. Over the course of the lease, the market for their space appreciated 65%, reaching a high of ~$87.50 (this would have been January of 2020). When the pandemic hit the market decline began at $87.50, not $53. Today direct asking rents are off about 12%. So the current market value for this space is in the upper $70s; whereas the tenant’s rent, after annual increases, is likely in the mid $60s. Adding to this is the fact that in San Francisco, direct availability (not sublease) is about 10%. This is why direct lease rates are only off about 12%. Sublease space accounts for 45% of available supply. These 2 markets (sublease vs. direct) perform differently as the parties have significantly different motivations. The sublandlord is looking to mitigate cost as quickly as possible and the landlord is looking to preserve or enhance asset value.

A Short Discussion of Operating Expenses and Taxes (Insert Big Yawn Here)

I know. This is painful. But you need to understand it, so here goes. A third or more of a tenant’s occupancy cost is attributed to the operation and taxation of the building in which it leases space. Yet these costs and how they are distributed are often a source of confusion.

Firstly, there are several ways in which landlords deal with these expenses. In San Francisco, for most class A buildings, the common approach is what is known as a full-service, gross lease with a Base Year. In this case, the Base Year is established during the negotiations, typically the year in which the new lease commences; provided, however, if the lease starts in the 2nd half of the year, the Base Year is often pushed to the following calendar year. In simple terms, during the Base Year, the tenant pays only its Base Rent. So, for example, if the Base Rent is $70/sf, it only pays $70/sf. The total amount of operating expenses and real estate taxes for the full calendar year, less any excluded items, is then established as the Base Year amount. For example, if the operating expenses total $18/sf and the taxes are $5/sf, the total Base Year value is $23/sf. The tenant then pays its pro rata share of any increases above these amounts as such increases may occur in subsequent lease years. So if operating expenses go from $18/sf to $18.50/sf, the tenant is responsible for the $.50/sf increase. If the tenant occupies 10,000 sf, that translates to $5,000 in additional operating expense costs for that lease year. Similarly, if taxes increase, the value of the increase is passed on to the tenant. Under this lease structure, the building management team will project future increases at the end of a given calendar year and in the next calendar year, charge the tenant the estimated monthly value of the projected increases. At the end of that year, management will “true up” the costs and either bill the tenant for any shortfall or credit back any overage.

Another common approach to leasing is what’s known as a NNN lease. In this lease structure, the tenant pays all operating expenses and taxes. It pays a Base Rent, which is usually lower than the Base Rent you find in a gross lease since the tenant is picking up all the expenses and taxes. So if the space in our prior example was leased as a NNN lease, it would likely have a Base Rent of $47/sf and a total year one NNN rent of $70/sf. The operating expenses and taxes would be the same (e.g., $23/sf) but they would be passed on to the tenant in full from day one. In subsequent years, the cost would increase based on the extent to which the lease calls for Base Rent increases and the extent to which the operating expenses and taxes increase. NNN leases can end up being a little less costly than Gross Leases because the annual Base Rent increases are done from the Base Rent value, not the fully-serviced rent. In the first example, where the starting rent is $70/sf if there is a 3% annual rent escalation, it is calculated off the $70/sf rate; whereas in the case of the NNN lease, the annual rent escalation is calculated off the $47/sf rate.

There are numerous other variations of the concept. For example, some leases are NOE, which stands for Net of Electricity. And there are leases which are NUJ, or Industrial Gross, both of which are net of utilities and janitorial.

It’s no wonder this can be confusing. Adding to the confusion is the negotiation around what should be included and excluded in the calculations. A good real estate advisor will be well-versed in all the different ways in which expenses and taxes are treated and will be able to successfully negotiate appropriate exclusions. This is but one of the seemingly obscure areas in which a tenant seeking to negotiate on its own is likely to miss the opportunity to mitigate costs.

The Math Behind the Motivation

Occupiers often think pricing for office space is one dimensional. Sure, they understand that different quality buildings and spaces translate to different prices. But pricing is actually complex and dynamic, based on many variables, including specific owner motivations. And motivations vary significantly from one owner to the next.

Consider the exact same quality of space in 2 comparable buildings having different owners. On the surface, you might expect the owner’s rental objectives to be similar. However, in practice, they can be drastically different. Why? Because owner motivations and the leverage narrative may be completely different. How can they differ? Start with the asset itself. How much of the building is vacant or soon to be vacant? What percentage of the leases roll in the near-term? What is the owner’s cost basis? Does the owner intend to hold the asset for the long term, or will they look to sell? Is the asset evaluated on a stand alone basis, or is it part of a portfolio? Is the owner a REIT?

It’s not uncommon to see a situation in which one owner is willing to transact for $65/sf; whereas the other won’t transact for anything less than $75/sf. For the existing tenant, seeking to execute a discounted lease extension, the normal approach is to leverage the value it creates by de-risking the owner’s future. Specifically, the extending tenant will often require less capital (tenant improvements) and will not expose the owner to a disruption in cash flow. However, even when the cash flow from the discounted extension of the existing tenant is higher than that from a new deal at full market, the owner whom is focused on max valuation will go for the higher rent, riskier outcome. This is because they’ll make more profit on the sale due to a higher asset value. Commercial office buildings are valued based on the capitalization of net operating income. A $10/sf swing in net operating income at a 5.5% cap rate is worth $181/sf in asset value. If we’re evaluating a 20,000 sf space, that’s worth $3.6M. Even if the owner has to spend $50/sf more in tenant improvements and the space sits vacant for 12 months, the value derived from a future sale is greater than the cost of acquiring the new deal, which is about $2.3M (the additional $50/sf in TI and the 12 months downtime). Further, holding firm on rental value may have an aggregate effect on the values of other space in the asset. So while the owner takes more risk and spends more up front, it comes out $1.3M ahead. Now consider this same calculus over a 600,000 sf asset.